The trade started at five in the morning. The name on it was decided after lunch.

The SEC says Stephen Leech ran more than $600 million of losing trades into the conservative bond funds where ordinary Americans parked their retirement money. Western Asset agreed this week to pay $100 million. The trades were placed at dawn. The names were filled in after the prices moved.

Marguerite kept the statements in a manila folder on the second shelf of the kitchen desk, behind the one labeled TAXES and in front of the one labeled HOUSE. She was sixty-eight. She had been a school librarian in Pasadena for thirty-one years before she retired, and she had rolled her 403(b) into an IRA at a discount broker the year her husband died. The broker had asked her how she wanted it allocated. She had said the word she had been taught to say. Conservative.

A piece of that money sat in a Western Asset fund called Core Plus. It was a bond fund. Bonds were the safe part. That was the deal.

She did not know that the building where her money lived was in Pasadena too, four miles from her kitchen.

She did not know what time the trades got made.

I.

A cherry-picking scheme is a quiet one. It does not require a fake company or a fake auditor. It requires only a delay.

Here is how the SEC describes what happened, in plain language. A portfolio manager places a trade in the market in the morning. He does not yet say which client account the trade belongs to. The trade sits in what is called an omnibus account, which is a single bucket holding orders before they get assigned. The manager waits. He watches the price move during the day. By the afternoon, he knows whether the trade has made money or lost money on its first day. Only then does he tell the back office whose account to put it in.

If the trade made money, it goes to the favored client.

If the trade lost money, it goes to the disfavored one.

The favored client gets a quietly excellent year. The disfavored client gets a quietly bad one. Neither of them knows there was a choice.

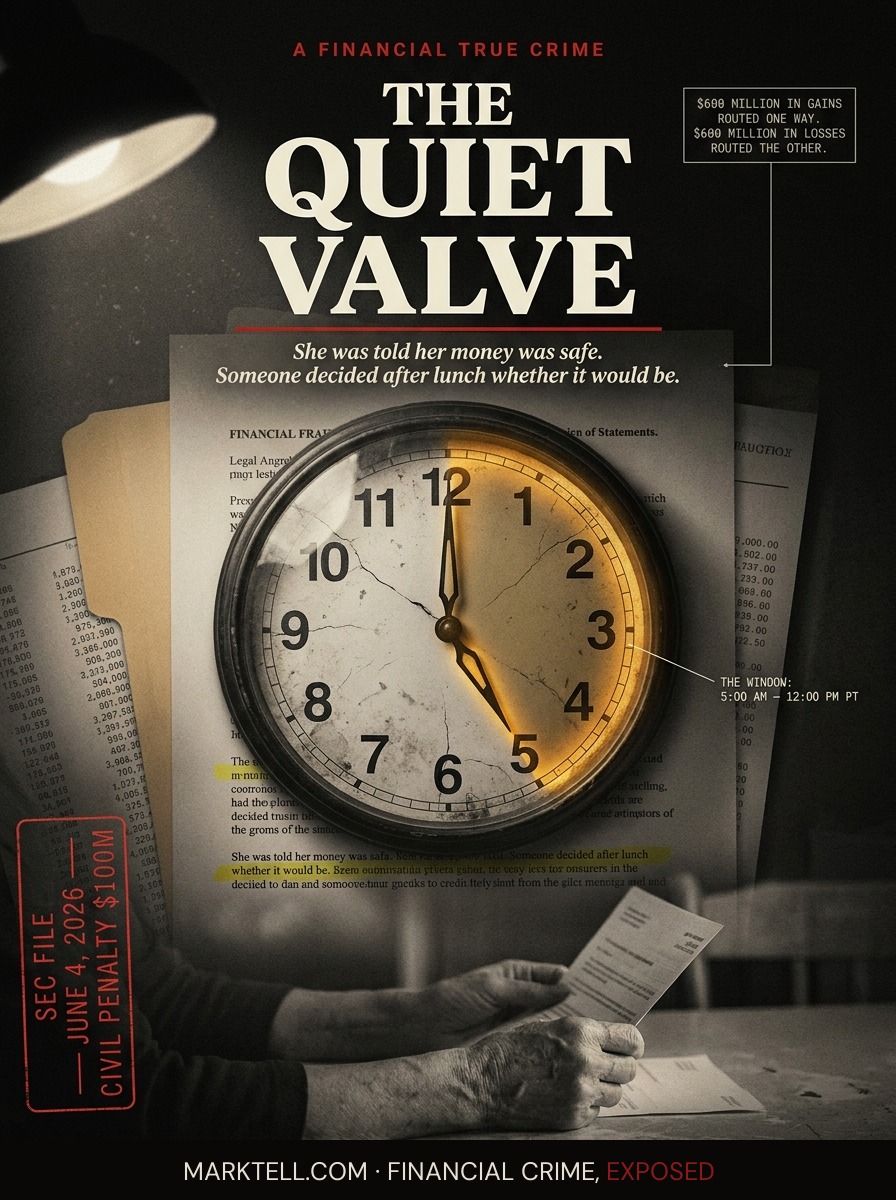

According to the SEC's order, that is what Stephen Kenneth Leech II did from January 2021 through October 2023. Leech, 71, was at the time co-Chief Investment Officer of Western Asset Management, the fixed-income unit of Franklin Resources. He placed trades as early as 5:00 a.m. Pacific. He routinely waited until after 12:00 p.m. Pacific, after settlement prices were visible, to send the allocation instructions.

The favored side was a strategy called Macro Opportunities. The disfavored side was Core and Core Plus.

Read that slowly. The strategy called Macro Opportunities is the one investors choose when they want to take risk. Core and Core Plus are the strategies investors choose when they do not. The names are the promise.

The SEC says Leech sent more than $600 million of first-day gains one way, and more than $600 million of first-day losses the other.

Marguerite was on the other side.

II.

The settlement was filed on June 4, 2026. Western Asset agreed to pay a $100 million civil penalty, accept a formal censure, and accept a cease-and-desist order. The firm did not admit and did not deny the SEC's findings. Franklin Resources, the parent, disclosed the penalty in a Form 8-K the next day. The penalty money will go into what is called a Fair Fund, which is the pot the SEC uses to pay back the people who were harmed. The people who were harmed are the people who held Core and Core Plus.

The SEC found that Western Asset willfully violated two anti-fraud provisions of the Investment Advisers Act of 1940. Section 206(2). Section 206(4). It also found that the firm violated Rule 206(4)-7, which is the rule that requires investment advisers to have written compliance policies that actually work, and that it failed to reasonably supervise Leech.

Leech himself is in a different proceeding. The Department of Justice has charged him criminally. He has pleaded not guilty. That case is ongoing. Allegation is not adjudication. He is presumed innocent of the criminal counts.

But the civil findings against the firm are now in the record.

III.

Picture the room. Not the trading floor, which has been on television. Picture the smaller room, where allocation instructions get sent. A few screens. A back office. A spreadsheet. A clock on the wall that says it is afternoon.

By afternoon, the morning is no longer a question. The bonds have either moved up or moved down. The Treasury auction has either gone well or gone badly. The thing that was uncertain at five in the morning is, by one in the afternoon, a fact.

That is the window the SEC says Leech used. The hours between the uncertainty and the fact. The valve sits in that window. Open it one way, and the gain flows to Macro Opportunities. Open it the other way, and the loss flows to Core Plus. The valve does not look like fraud. It looks like an instruction.

This is what makes cherry-picking hard to see from the outside. It does not leave a missing dollar. The dollar is there. It is just in the wrong account. The favored fund's performance looks earned. The disfavored fund's performance looks like the market.

Marguerite read her statement at the kitchen table with a yellow highlighter and could not figure out why her conservative allocation was dragging. She did what the magazines told her to do. She compared it to the benchmark. She held on. She told herself bonds were having a bad stretch. Bonds were having a bad stretch. That was true. It just was not the only thing that was true.

IV.

The investigation became public in August 2024. Leech was placed on leave. He later stepped down. What happened next is the part of the story the industry will remember.

Approximately $120 billion left Western Asset between August 2024 and January 2025. That is not a typo. One hundred and twenty billion dollars walked out of the firm in five months. By December 2024, Western Asset's U.S. assets under management had fallen to roughly $179 billion. Franklin Resources, in its own filings, called it a "dramatic reduction." That is the corporate phrase. The plain phrase is that institutional clients, pension funds, the people who allocate other people's retirement money, read the disclosure and decided they did not want to find out which side of the valve they had been on.

Retail clients like Marguerite are slower. They do not have a chief investment officer who reads the SEC docket on Monday morning. They have a quarterly statement that arrives in the mail and a kitchen table and a manila folder.

This was not Western Asset's first SEC matter. In 2014, the firm paid more than $21 million to settle SEC charges related to concealing losses and improper cross-trades in client accounts. The 2014 settlement involved different conduct. But the category is the same category. Allocation. Disclosure. Which client got which trade.

Two settlements, twelve years apart, both about the question of who ended up holding what.

V.

The thing to understand about a fiduciary is that the word is not decorative. It is a legal status. An investment adviser registered under the 1940 Act owes its clients a duty of loyalty and a duty of care. The duty is not to make money. The duty is to put the client's interest first. To allocate fairly. To disclose conflicts. To not, under any circumstance, decide after the fact which client gets the winner and which client gets the loser.

A cherry-picking scheme is, in the SEC's framing, a violation of that duty at its most basic level. It is not a bad bet. It is not a market call gone wrong. It is the manager keeping the upside for the account he wants to favor and routing the downside to the account he does not. The harm is not that the trade lost. The harm is that the loss was assigned, in retrospect, to a specific person who was told her money was being managed for her.

Marguerite was being managed for. That is what the prospectus said. That is what the word "conservative" meant. That is what the manila folder, behind TAXES and in front of HOUSE, was built on.

VI.

There will be a Fair Fund. The $100 million will be deposited into it and a claims administrator will figure out, account by account, who held Core and Core Plus during the relevant period and what the harm was. Marguerite will probably get a letter. The letter will probably arrive in the same mailbox where the statements used to come. She will probably open it at the kitchen table.

The math the letter shows will not be the whole math. It will not include the years she spent thinking she had done something wrong. It will not include the conversation she had with her broker about whether to switch funds, the one where she decided to be patient because patience was supposed to be the virtue. It will not include the trust, which is the part you cannot rebate.

The SEC has called cherry-picking a priority. It uses an internal tool called the National Exam Analytic Tool, NEAT, to look at allocation patterns across advisers' books. It is looking for exactly this. A pattern in which the timing of allocation instructions correlates, too neatly, with the direction of the day's price move.

The pattern is hard to hide from a regulator with the right software. It is impossible to see from a kitchen table.

That part may be the saddest. The mechanism was not subtle to the people who knew where to look. It was only subtle to the people who were inside it.

The trade started at five in the morning. The name on it was decided after lunch. For three years, the name on the losing ones was hers.

- SEC Order, In the Matter of Western Asset Management Company, LLC | June 4, 2026 | SEC administrative proceeding

- Franklin Resources Inc. Form 8-K | June 5, 2026 | SEC EDGAR

- InvestmentNews, "Western Asset agrees to $100M SEC penalty over cherry-picking scheme" | June 2026

- DOJ criminal complaint and indictment, United States v. Stephen Kenneth Leech II | 2024-2026 | ongoing

- SEC press release on Western Asset settlement | June 2026

- SEC 2014 settlement with Western Asset Management Company (prior matter) | 2014

- Investment Advisers Act of 1940, Sections 206(2), 206(4), and Rule 206(4)-7

- Franklin Resources public disclosures on Western Asset AUM, August 2024 - January 2025

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.