The receivables grew. The growth did not. That gap is the case.

A short seller said ADMA's 20% growth was really a 3% decline hidden in distributor warehouses. The stock fell 29% in two days. Now the lawsuits are stacking up.

Marlene checked the app at 6:47 AM in the hospital breakroom, before her shift, the way she always did. Coffee in a paper cup. Phone flat on the counter. She is sixty-two. She has been a pharmacy tech for thirty-one years, most of them at the same suburban Ohio hospital, and when she rolled her 401k two years ago she put a slice of it into ADMA Biologics because ADMA made plasma-derived medicine for kids with weak immune systems and she had seen what that medicine did on the pediatric floor. She bought the story before she bought the stock. That is how this works.

The ticker was red. Not a normal red. The kind of red that does not fit on the line.

She did not know yet that a short seller named Culper Research had published a report the previous evening with a title that read more like an indictment than a research note: "ADMA Biologics Inc (ADMA): Channel Stuffing, an Undisclosed Related Party Distributor, and –3% Real Growth in 2025 vs. +20% Reported." She did not know yet that by Wednesday's close her position would be worth about seventy cents on the dollar of what it had been on Monday. She just saw the red. She put the phone face-down and went to work.

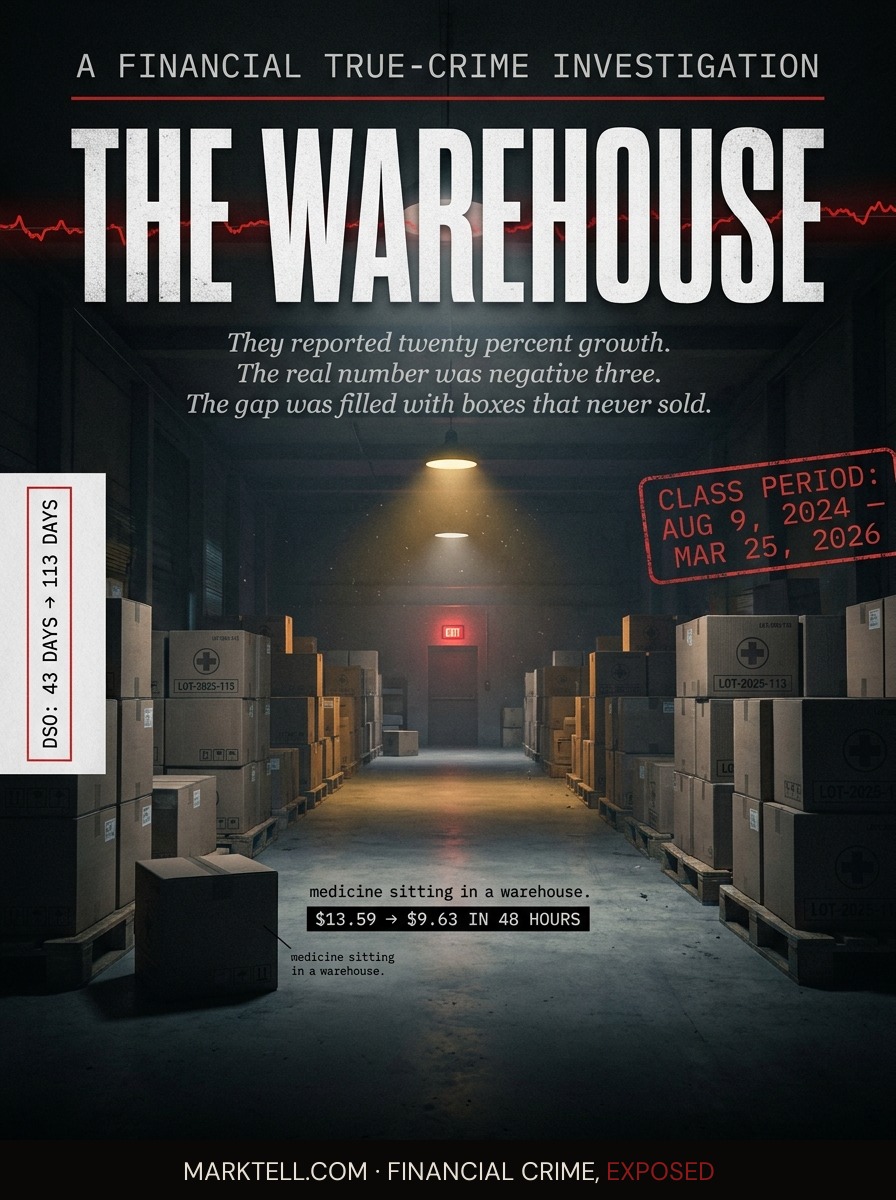

This is a story about a warehouse. Not a real one. A conceptual one. The warehouse is where you put the growth you did not actually have.

I.

ADMA Biologics is a real company with a real product. ASCENIV is the flagship: an immune globulin therapy approved for primary humoral immunodeficiency. On May 4, 2026, the FDA expanded its label to include pediatric patients two years of age and older. That is not a fake business. That is the part of the story that made Marlene buy.

But somewhere between the medicine and the market, according to the class action filed in 2026 and the Culper Research report that set it off, something else was happening.

The lawsuit, Mazzarino v. ADMA Biologics, covers investors who bought ADMA stock between August 9, 2024 and March 25, 2026. The complaint alleges that during that period the company's reported revenue growth was not what management said it was. Reported 2025 growth: +20%. The growth Culper says was real: –3%. The gap, according to the allegations, was filled by pushing product out to distributors faster than distributors could sell it, and counting the shipments as revenue.

That is what channel stuffing means. You ship more than the customer needs. The customer is your distributor, not the patient. The distributor takes it because you give them long payment terms and they have nowhere to push back. You book the sale. The number on the earnings release goes up. The medicine sits in a warehouse.

Read that again. The medicine sits in a warehouse. That is what the growth was.

II.

Here is the part the filings let you see without taking anyone's word for anything.

Days Sales Outstanding. That is the average number of days it takes a company to collect cash after it makes a sale. A low DSO means customers are paying quickly. A rising DSO means cash is sitting on someone else's loading dock.

According to Culper Research's analysis of ADMA's public filings, DSO went from 43 days to 113 days in 2025. That is not a drift. That is a doubling and then some.

Two distributors, BioCare and CuraScript, accounted for 73% of revenue and 87% of year-end receivables, per the Culper report. Payment terms had allegedly been extended to 120 days, against a more typical 30. Distributors were allegedly holding four to six months of inventory. Normal is closer to thirty days.

Picture it. A warehouse with four to six months of plasma product. A receivable on ADMA's books that the distributor will not pay for 120 days. A press release that says the company grew 20%.

The press release gets the headline. The DSO gets the 10-Q footnote. The patient gets the medicine eventually. The shareholder gets the stock price built on the assumption that the headline is the same thing as the business.

There is a second allegation, and it is the one that makes a securities lawyer's pen come uncapped. The complaint alleges ADMA failed to disclose a material related-party distribution relationship with an entity called Genesis BioPharma Services. A related party is exactly what it sounds like: someone connected to the company in a way that needs to be disclosed because it changes how you read the numbers. If your biggest customer is also your cousin, the investor needs to know.

ADMA, for its part, has called the allegations "unsubstantiated, misleading and inaccurate." Cantor Fitzgerald, an investment bank that had been bullish on the stock, downgraded ADMA to Neutral on March 26, 2026. The downgrade note specifically cited the company's response, or absence of a detailed one, as a concern. None of the allegations have been adjudicated. The case is in front of a judge. The lead plaintiff deadline is August 10, 2026.

I am writing this in June 2026. We will see what the discovery says.

III.

Marlene came home Tuesday night and opened the app again. ADMA had closed at $11.33, down $2.26 from the day before. A 16.6% drop. She had told herself in the breakroom that morning she would not check again until the weekend. She checked again Tuesday night.

Wednesday she did not check from the breakroom. She checked from the parking lot. $9.63. Down another 15%. The two-day damage came to roughly 29%, from $13.59 on Monday's close to $9.63 on Wednesday's. Her rollover slice, which had been north of forty thousand dollars on Monday morning, was something like twenty-eight thousand by Wednesday afternoon.

She did not call anyone. She did not sell. She is sixty-two and she has been working nights for three decades and she has learned not to make decisions on a parking-lot phone at 7 PM after a twelve-hour shift.

That part may be the saddest. Not the loss. The discipline.

IV.

The defense, when it comes, will be the one these defenses always are.

The defense will say the inventory build was strategic. The defense will say the relationship with Genesis BioPharma Services, if material, was disclosed elsewhere or was not material. The defense will say the DSO increase reflected legitimate commercial decisions in a complicated plasma market. The defense will point to the ASCENIV pediatric label expansion as proof that the underlying business is real. The defense will note that the long-term guidance, which targeted over $1.1 billion in revenue by 2029, was withdrawn in May 2026 because of "market dislocation," not because the growth was a story.

Some of that may be true. The plasma business is real. The medicine is real. The pediatric approval is real.

But the question the complaint is asking, and the question the discovery process will try to answer, is whether the gap between +20% reported and –3% real was filled by a warehouse instead of a customer. The question is whether the receivables grew because the business grew or because the receivables had to grow to keep the business looking like it grew.

Not the exciting questions. Not the TV questions. The ugly questions. The 10-Q questions. The kind of questions Marlene cannot ask from a hospital breakroom and that her broker did not ask before she bought.

V.

What ADMA Biologics is accused of, if the allegations hold, is not exotic. Channel stuffing is one of the oldest mechanisms in corporate accounting. Sunbeam did it. Bristol-Myers Squibb did it. McKesson did it. The SEC has a whole shelf of resolved cases that look like this one in outline: a company under pressure to hit a number, a distributor willing to take more than it can sell, a payment-terms extension hidden in a footnote, a DSO line that climbs while everything else looks fine.

The warehouse is the machine. The medicine is the cover. The DSO is the fingerprint.

You can see this one without having to take Culper Research's word for it. You can pull the 10-K. You can look at the receivables. You can read the customer concentration disclosure. The 43-to-113 jump is in the filings. The 73% revenue concentration is in the filings. The press release that said +20% is in the filings.

What is not in the filings is the relationship with Genesis BioPharma Services. That is the part the complaint says was hidden. That is the part discovery will try to pull into the light.

VI.

Marlene is still in the position. She is still working nights. The pediatric floor still uses the medicine. ASCENIV still works for the kids it works for. None of that is the case.

The case is whether the people who bought the stock between August 9, 2024 and March 25, 2026 were sold a number that the company knew was not the number. The case is whether the warehouse counted as growth.

She bought the medicine. She got the warehouse.

That is what the receivables tried to tell her, eighteen months before Culper Research published the PDF.

The footnote was already there. Nobody was reading it.

- Culper Research | March 24, 2026 | "ADMA Biologics Inc (ADMA): Channel Stuffing, an Undisclosed Related Party Distributor, and –3% Real Growth in 2025 vs. +20% Reported"

- Mazzarino v. ADMA Biologics, Inc., et al. | 2026 | Class action complaint, BFA Law (Bleichmar Fonti & Auld LLP)

- ADMA Biologics | May 6, 2026 | Q1 2026 earnings release and guidance update

- FDA | May 4, 2026 | ASCENIV pediatric label expansion approval

- Cantor Fitzgerald | March 26, 2026 | Analyst downgrade note, ADMA to Neutral

- FinancialContent / GlobeNewswire | June 2026 | BFA Law investor notice press release

- ADMA Biologics | 2024-2026 | 10-K and 10-Q filings, SEC EDGAR

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.