The promoter paid $1.7 million. The retirees who bought the shares paid the rest.

A federal court ordered a penny stock promoter tied to the Barry Honig ring to pay $1.7 million for his role in a long-running pump-and-dump. The number is real. So is the retiree in Ohio who held the shares when the music stopped.

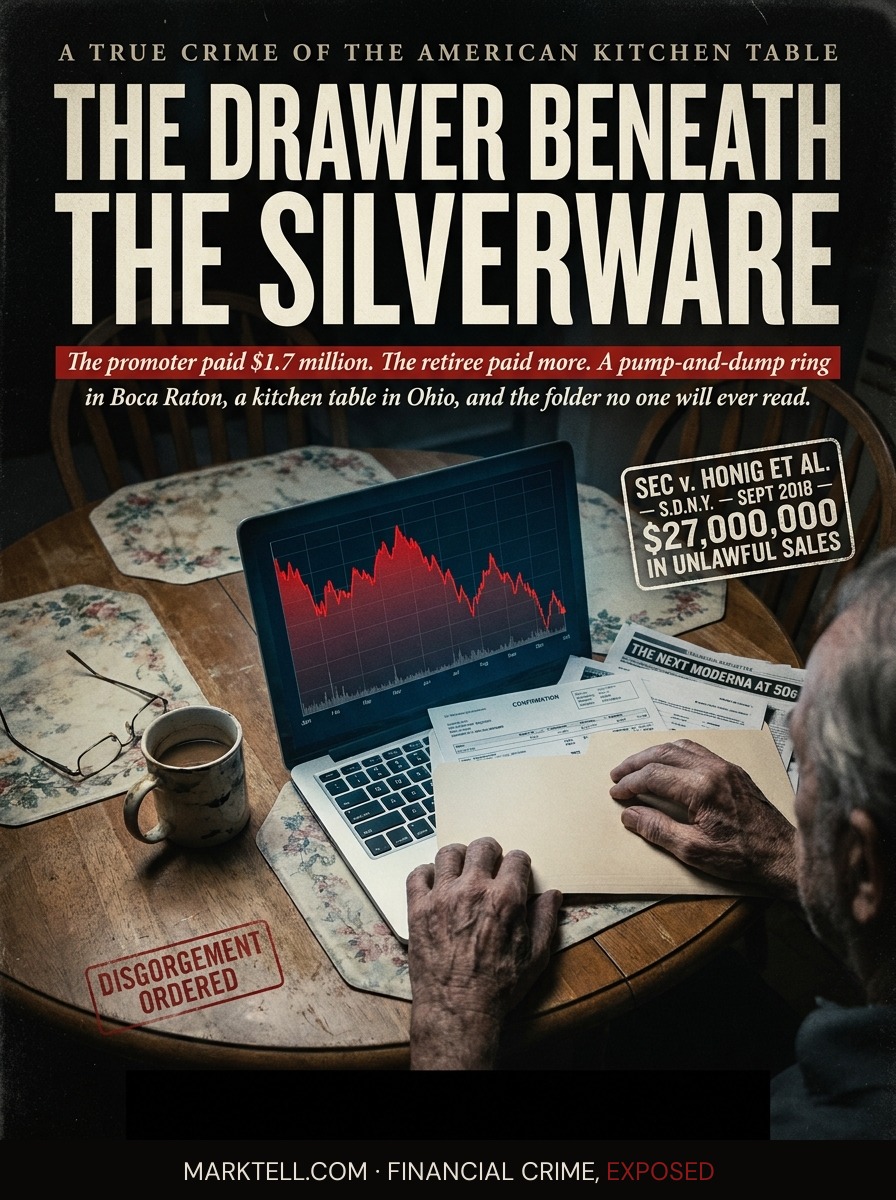

Glenn is seventy-one and the kitchen table is where the trades happen. The laptop sits on a placemat his wife bought at a church bazaar in 1994. The television in the next room runs CNBC with the sound off, because the sound is for people who still believe what people on television say. Glenn does not. Glenn reads.

He reads small-cap newsletters. He reads message boards. He reads the kind of email that arrives on a Tuesday and tells him a clinical-stage biotech is about to announce something the big funds do not know yet. He retired from a tool-and-die shop outside Mansfield, Ohio in 2014. He has a pension that does not stretch and a curiosity that does. The curiosity is what the machine eats.

On a morning that could be any morning between 2013 and 2018, Glenn buys two thousand shares of a company he had never heard of three weeks earlier. The ticker is on the OTC market. The price is under a dollar. The newsletter calls it "the next Moderna at fifty cents." Glenn does not buy the next Moderna. Glenn buys a position in a stock whose float is already owned by people he will never meet, in an office he will never see, in Boca Raton.

That is the room. That is the chapter.

I. The Boca Raton room

The U.S. Securities and Exchange Commission filed a civil complaint in September 2018 in the Southern District of New York. The lead defendant was Barry C. Honig of Boca Raton, Florida. The complaint named ten individuals and ten associated entities. The SEC alleged the group ran coordinated pump-and-dump schemes from 2013 to 2018 and generated over $27 million in unlawful stock sales.

A pump-and-dump is the oldest small-stock fraud there is. You buy a large block of a thinly traded stock cheap. You promote the stock loudly. You sell into the buying you created. The buyers are people like Glenn.

The SEC's complaint described how the ring allegedly acquired the discounted shares first, then directed promotional activity, then sold their inventory into the demand they had manufactured. Sanjay Wadhwa, then a senior official in the SEC's Division of Enforcement, called it "brazen market manipulation."

The tickers in the complaint included BioZone Pharmaceuticals, MGT Capital Investments, and PolarityTE. Glenn does not know any of those names by heart. He knew them for two weeks. Then he knew them as losses in a tax document.

II. What a settlement looks like

A settlement in a case like this is not a confession. It is a number.

Phillip Frost, the Miami biotech billionaire named in the complaint, settled for $5.52 million. Mark Groussman settled for $1.38 million. Michael Brauser, John O'Rourke III, and John Stetson were ordered to pay disgorgement, prejudgment interest, and civil penalties of $1,175,176, $1,153,326, and $1,154,669 respectively, according to court filings in 2020. Honig agreed to a bifurcated settlement in June 2019. He accepted a ban on investing in or financing publicly traded small-cap companies. The dollar number was left to be litigated later.

This week the number is $1.7 million. A penny stock promoter inside the ring has been ordered to pay $1.7 million. Bloomberg Law News reported it on Tuesday. The court did the work the SEC asked it to do.

Read that slowly. $1.7 million is the disgorgement number. It is not the amount Glenn lost. Glenn's loss is in a different ledger. Glenn's loss is the fuel. The $1.7 million is what the regulator could claw back from the people who burned it.

III. Glenn at the table

Go back to the kitchen.

The trade confirmation arrives. Glenn prints it. He puts it in a manila folder he keeps in the drawer beneath the silverware. The folder has other confirmations in it. Some of them are winners. Most of them are not. He does not tell his daughter Sarah about the folder because Sarah would not understand why he keeps trading. Sarah thinks he should be in an index fund. Glenn thinks the index fund is for people who have given up.

The stock spikes. Glenn checks the chart on his phone in the Kroger parking lot. He is up forty percent. He thinks about selling. He does not sell. The newsletter said the catalyst has not been announced yet.

The catalyst is not coming. The catalyst was never coming. The catalyst was the promotion itself. When the promoters stop promoting, the catalyst stops. Glenn does not know this because Glenn does not know that the people writing the newsletter were paid in the same shares Glenn is now holding.

The stock drops. Glenn waits. The stock drops again. Glenn waits. By the time he sells, the position is down sixty-eight percent. He puts the new confirmation in the folder. He closes the drawer.

That part may be the saddest. The folder. The closing of the drawer.

IV. The mechanism, named

The SEC complaint described the moving parts. They are worth saying in plain language.

The ring allegedly bought stock at deep discounts in private placements. That means they got shares cheaper than anyone in the public market could get them. They allegedly arranged for promoters to write favorable coverage without disclosing the promoters were paid. They allegedly used nominees and fake names so the size of their position would not be visible. They allegedly placed buy orders among themselves to create the illusion of organic trading volume. Then they sold.

Each of those pieces is a step. Together they are a machine. The machine has been running in some form since at least the 1980s, when I sat in a room in Chicago selling shares in a company that made stock certificates instead of blimps. The machine does not care about the product. The machine cares about the float, the volume, and the exit.

The press release gets the screenshot. The complaint gets the docket number. The newsletter gets forwarded. The Form 4 filings get ignored. The chart gets the rocket emoji. The 10-Q gets the silence.

V. The Supreme Court, quietly

On June 4, 2026, the Supreme Court ruled unanimously in Sripetch v. SEC that the Commission does not have to prove that investors suffered measurable financial loss in order to obtain disgorgement in enforcement cases. That ruling is three weeks old as of this writing.

What that means in plain English: the regulator no longer has to walk a court through Glenn's folder to take the money back from the people who made the trades. The ill-gotten gain is the ill-gotten gain. The court can order it returned without auditing the kitchen table.

That is why this week's $1.7 million number landed the way it did. The disgorgement tool got sharper this month. The court used it.

VI. What Glenn never learned

Glenn does not read Bloomberg Law News. Glenn reads small-cap newsletters and the AARP magazine and the obituaries in the Mansfield News Journal. He will not see the $1.7 million number. He will not know that a court in the Southern District of New York ordered a man in Boca Raton to disgorge money that, in some chain of cause and effect that no court will trace, started in the drawer beneath his silverware.

He will get another newsletter next month. The newsletter will be about a different ticker. The ticker will be on the OTC market. The price will be under a dollar.

The room in Boca Raton has been closed. Other rooms are open. Bloomberg's own analysis identified roughly seventy small public companies showing pump-and-dump trading patterns, with an estimated $16 billion in market capitalization wiped out. Seventy rooms. Sixteen billion dollars. One Glenn, multiplied.

VII. The number that is not the number

$1.7 million is the headline. It is a real number. It is a court-ordered number. It belongs in the record and the record matters.

But Glenn's number is not in the record. Glenn's number is in the folder in the drawer.

The promoter paid. The retiree paid more.

- SEC Press Release | September 7, 2018 | SEC charges Barry Honig and associates with fraudulent pump-and-dump schemes, U.S. District Court for the Southern District of New York

- SEC Litigation Release | June 2019 | Bifurcated settlement with Barry C. Honig

- SEC Litigation Release | March 2020 | Final judgments against Michael Brauser, John O'Rourke III, and John Stetson

- SEC Press Release | various | Settlements with Phillip Frost ($5.52M) and Mark Groussman ($1.38M)

- Bloomberg Law News | June 23, 2026 | Penny Stock Promoter Must Pay $1.7 Million Over Pump-and-Dump

- Sripetch v. SEC | June 4, 2026 | U.S. Supreme Court ruling on disgorgement standard

- Bloomberg | analysis of pump-and-dump trading patterns across approximately 70 small public companies

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.