The promissory notes were on letterhead. The bonds did not exist.

Edwin Emmett Lickiss, Jr., 78, of Danville, pleaded guilty this week to running a Ponzi scheme that lasted from 1998 to 2024 and took at least $9.5 million from more than 93 investors. The license he needed to do any of it was gone by 2016.

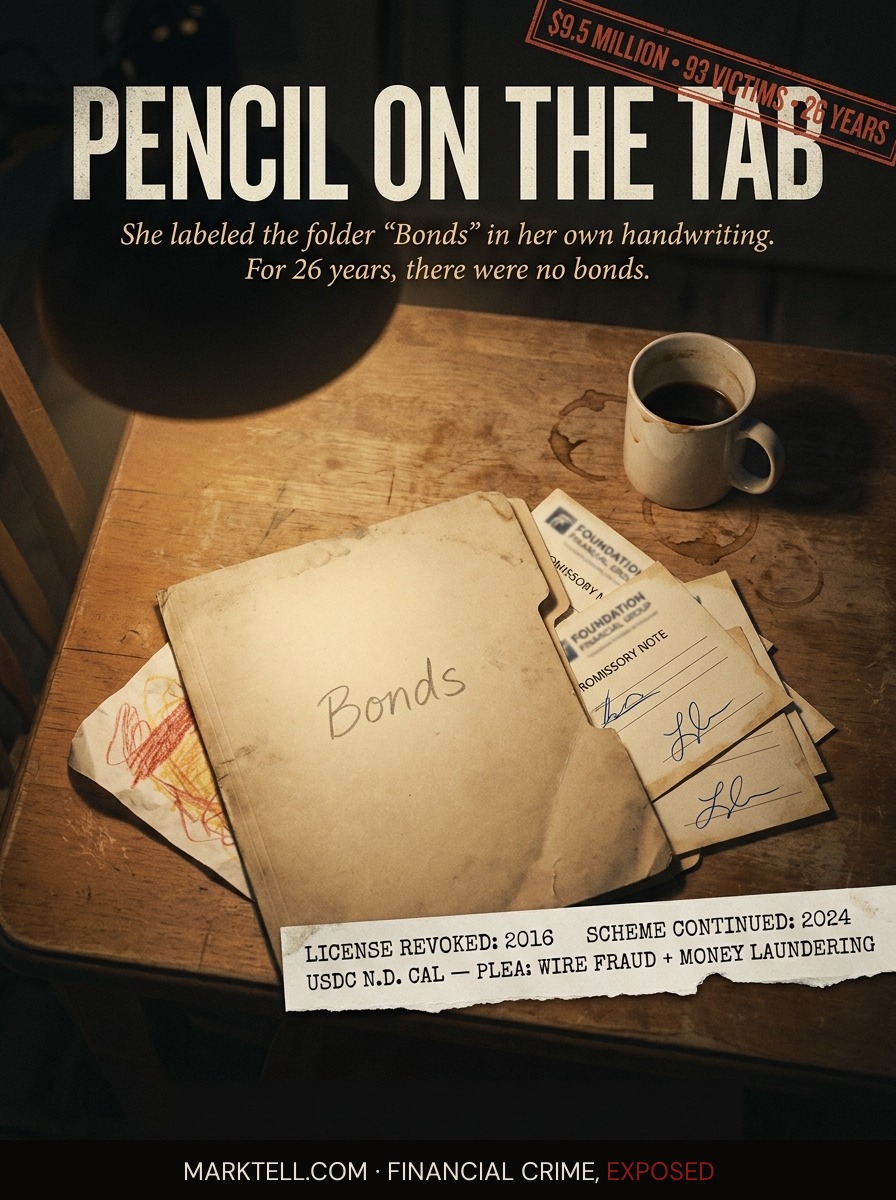

The folder was labeled "Bonds." Marilyn had written it herself, in pencil, sometime around 2006. She was seventy-one now. The folder lived in the second drawer of the kitchen desk in her Walnut Creek house, behind the warranty paperwork for the dishwasher and a stack of cards her grandchildren had drawn.

Inside the folder were promissory notes printed on letterhead. Foundation Financial Group. Danville address. A logo that looked the way a logo is supposed to look. Each note carried Edwin Lickiss's signature in blue ink, the same loop on the L every time.

In September 2024, the quarterly check did not come.

Marilyn waited a week. Then two. She called the office number on the letterhead and got voicemail. She called the cell number Ed had written on the back of one of his cards, years ago, the card she kept clipped to the inside of the folder. Voicemail. She left a message and made coffee and sat at the kitchen table and looked at the folder.

That is where this story starts. Not in a courtroom. Not in a regulator's inbox. At a kitchen table in the East Bay with a folder labeled "Bonds" and a phone that no longer connected to the person who had been paying her for almost twenty years.

I.

Edwin Emmett Lickiss, Jr. is seventy-eight years old. He lives in Danville. On May 20, 2026, in federal court in the Northern District of California, he pleaded guilty to one count of wire fraud and one count of money laundering. According to the plea, he had been running a Ponzi scheme since 1998. He took at least $9.5 million from more than 93 investors. The scheme ran for twenty-six years.

A Ponzi scheme is a closed loop. The operator tells investors he is putting their money into something real. He is not. He is using new investors' money to pay old investors what they think are returns. The returns are not returns. They are other people's principal, passed through like a hand-off, with the operator keeping the rest.

Lickiss kept the rest.

The Department of Justice says he used investor money for cash withdrawals, home renovations, travel, and payments on vehicles, mortgages, and his personal credit cards. The court filings call these expenses what they are. The investors had called them returns on safe, tax-free bonds.

There were no bonds.

II.

The pitch was the part that worked. Lickiss told people he had access to exclusive bonds. Safe. Tax-free. Returns in excess of twenty percent.

Read that slowly. Safe. Tax-free. Over twenty percent.

A safe, tax-free bond paying over twenty percent does not exist. It has never existed. If it existed, every pension fund in the country would own it and nothing else. A bond that pays twenty percent is, by definition, not safe. The yield is the price of the risk. A bond that pays twenty percent and claims to be safe is a sentence describing something that cannot be in the room at the same time.

But Marilyn was not a bond trader. She was a retired school administrator. She had run a middle school in Concord for fifteen years and she had been very good at it. She understood budgets. She understood payroll. She did not understand fixed income markets, and she had never needed to, because Ed did.

That is the architecture. The mark does not need to know how the bond works. The mark needs to know the man who knows how the bond works. The trust is the product. The bond is the wrapper.

III.

Ed had been a real broker once. That part was true.

He was licensed. He had a firm. The firm had letterhead, and the letterhead had a logo, and the logo went on the promissory notes investors received in exchange for their checks.

In 2014, the Financial Industry Regulatory Authority, the self-regulatory body that licenses brokers, suspended his license. In 2016, FINRA revoked it. After 2016, Edwin Lickiss was not legally allowed to sell securities to anyone.

He kept selling securities anyway. For eight more years.

He kept issuing promissory notes on Foundation Financial Group letterhead. He kept taking checks from investors. He kept sending what he called interest payments. The Department of Justice calls these "lulling payments," which is the legal term for the money a Ponzi operator pays to old investors to keep them calm and quiet and willing to bring in more.

This is the part that should sit in the chest a moment. The license, the public credential that was supposed to mean something, was gone in 2016. The scheme continued through 2024. For eight years, anyone who looked Edwin Lickiss up on FINRA's BrokerCheck website, a free public database, would have seen that he was not licensed. For eight years, almost no one looked.

Marilyn did not look. She had no reason to. Ed had been to her husband's funeral in 2011. Ed had brought a casserole. Ed sat on her couch and explained, slowly and patiently, how the bonds worked, and Marilyn had written him a check for thirty thousand dollars in 2012 from the life insurance payout, and another check for fifty thousand dollars in 2017, and another in 2019.

The 2017 check, the 2019 check, the checks after 2016. Those were written to a man who legally was not allowed to take them.

IV.

The machine in this case is the letterhead.

A piece of paper. A logo at the top. An address in Danville and another in Alamo. A signature line. A loop on the L.

A licensed broker does not need letterhead. The license does the work. The license is the credential the regulator stands behind. When the license goes away, the credential goes away, and what is supposed to happen is that the operator can no longer write the notes, because the notes have nothing behind them.

What actually happened is that Edwin Lickiss kept the letterhead. He kept the office address. He kept the firm's name. He kept the signature. The visible surface of the operation looked exactly the way it had looked in 2013, when he was still licensed. Marilyn could not see the gap, because the gap was not on the paper. It was in a database she did not know existed.

The press release announcing the plea gets the light. The 2016 revocation gets the shadow. The promissory note gets the kitchen drawer. The unverified credential gets the assumption. The casserole at the funeral gets the trust. The eight years of unlicensed sales get the indictment.

V.

The FBI and IRS Criminal Investigation worked the case. Assistant U.S. Attorney Ben Wolinsky prosecuted. Sentencing is scheduled for August 28, 2026, before U.S. District Judge Jon S. Tigar. Lickiss faces a maximum of twenty years on the wire fraud count and ten years on the money laundering count. The statutory fine ceiling is $500,000 total. The actual sentence will be lower than the maximum. It always is.

The SEC has filed a separate civil enforcement action. That track will run on its own timeline. Restitution will be calculated. There will be a fight, as there always is, over how much of the $9.5 million can be recovered, because most of it has already been spent on the home renovations and the travel and the cars and the credit cards that the plea agreement describes.

The math on recovery in Ponzi cases is brutal. By the time the operator pleads, the money is gone. What remains is whatever assets the government can seize and liquidate. Investors who received "lulling payments" sometimes have to give those back, because the law treats those payments as fraudulent transfers from the broader pool of victims. The 93 people who trusted Edwin Lickiss are now in a line. Marilyn is in that line.

VI.

In October 2024, a month after the call that did not connect, Marilyn's son drove down from Sacramento. He sat at the kitchen table and went through the folder with her, one note at a time. He pulled up FINRA's BrokerCheck on his phone. He read what was on the screen, then read it again, then turned the phone so his mother could see it.

She asked him what it meant. He told her. She sat very still for a while.

Then she asked him not to tell his sister yet. Not until she figured out what to say about the grandchildren's college money, which was in the folder labeled "Bonds," which was now, the son explained gently, not in any bonds, and had not been in any bonds for a long time, and possibly never had been.

That part may be the part that sits longest. The folder was labeled in her own handwriting. She had been the one who wrote "Bonds" on the tab. She had named the thing she trusted, in pencil, and put it in the drawer, and the name had been wrong since the first check.

VII.

The pattern is older than Lickiss and it will outlive him. A licensed professional builds real relationships in a community. The license eventually goes away, for reasons the community does not see. The relationships remain. The letterhead remains. The trust, which was always the product, remains intact for years after the credential underneath it has been pulled.

Look up your adviser on BrokerCheck. It is free. It takes one minute. The url is brokercheck.finra.org. Type in the name. Read what the regulator says.

If the page shows a suspension, a revocation, a bar, a settled customer dispute, a criminal conviction, those are not paperwork issues. Those are the regulator telling you, in the only language the regulator has, what the people inside the system already know.

Edwin Lickiss had a revocation on his record starting in 2016. It was visible the whole time. The folder in Marilyn's kitchen drawer was labeled "Bonds." The page on the regulator's website was labeled something else.

She just did not know to look at the other label.

- U.S. Department of Justice, Northern District of California | May 20, 2026 | Press release on guilty plea of Edwin Emmett Lickiss, Jr.

- San Francisco Chronicle | May 2026 | "Ex-East Bay financial adviser admits to long-running Ponzi scheme"

- FINRA | 2014, 2016 | Broker license suspension and revocation records for Edwin Emmett Lickiss, Jr.

- U.S. Securities and Exchange Commission | 2026 | Civil enforcement action filed against Edwin Emmett Lickiss, Jr.

- Federal Bureau of Investigation and IRS Criminal Investigation | Investigative agencies of record

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.