The private shares were never private. They were never shares.

An Italian citizen running a New York investment advisory firm sold investors what looked like access to private company shares. Federal prosecutors say the shares did not exist. A judge sentenced him to four years.

Edward kept the folder in the second drawer down, the one with the brass pull that stuck in summer. Sixty-seven years old. Thirty-eight years pulling teeth in a strip mall office off the Saw Mill. He had retired the year before with a pension, a paid-off house, and a brokerage account that his wife described, accurately, as the thing he checked too often.

The folder was new. The folder was the smart money.

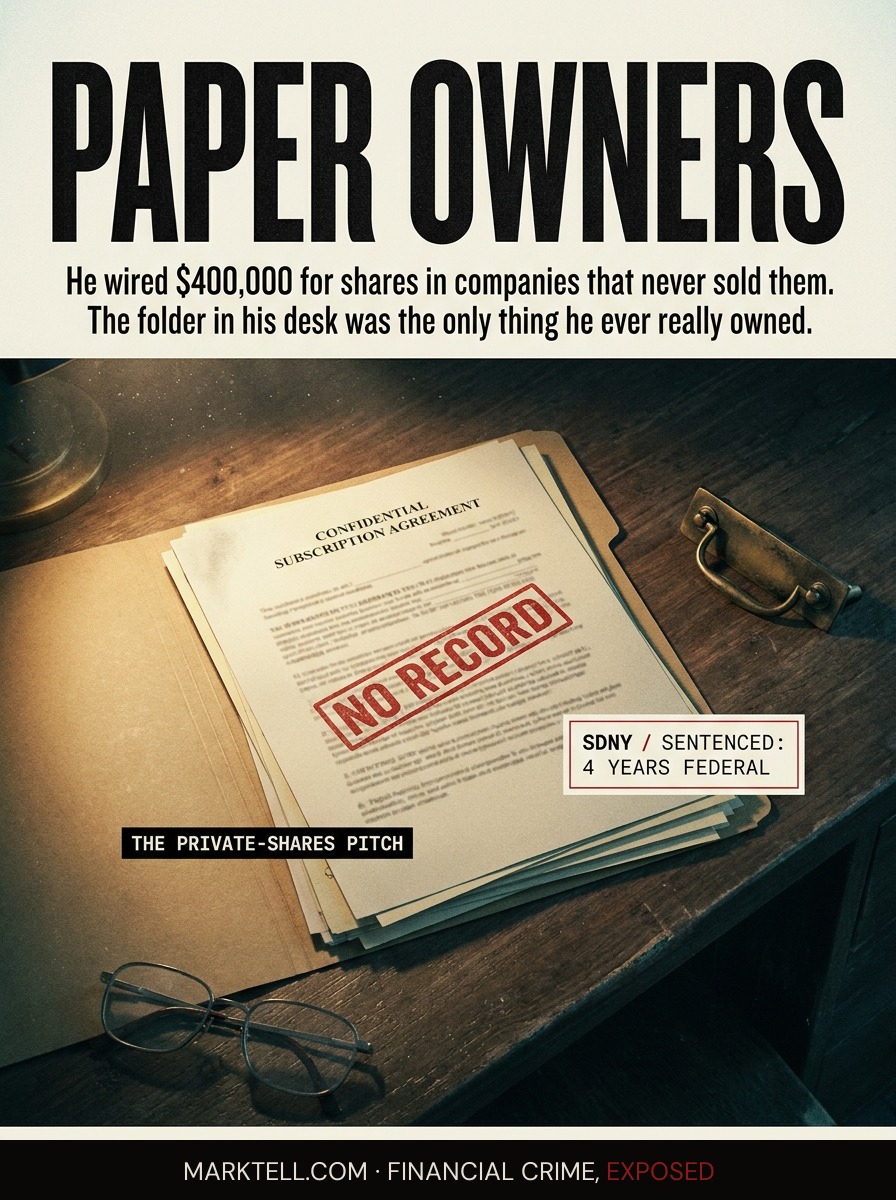

Inside it were six documents on heavy paper. Each one had a famous name at the top. Names you have heard. Names from the business section. Names with valuations in the tens of billions of dollars and no ticker symbol because they had not gone public yet. The documents called themselves Confidential Subscription Agreements. They were signed by Edward and countersigned by an adviser in Midtown who wore French cuffs and pronounced his name with the stress on the second syllable.

Edward had wired in just under four hundred thousand dollars. He thought he owned shares of companies that did not sell shares to people like him.

He owned paper.

I.

The pitch for private shares is the cleanest pitch in this business because the product is invisible and the customer wants it that way. A private company is a company whose stock is not traded on an exchange. You cannot buy it through your brokerage app. You cannot Google a price. The only people who own it are the founders, the employees who got it as part of their pay, and the venture capital funds that wrote checks early.

That exclusivity is the product.

The adviser does not have to show you a chart. He has to show you a door. He says he has access. He says, through a fund structure, through a special purpose vehicle, through a relationship, he can get you a sliver of the famous private company before it goes public.

You picture the IPO. You picture the morning the stock opens and the number on your statement triples. You picture telling your brother-in-law over dinner.

You sign at hour five.

II.

According to Law360, federal prosecutors charged an Italian citizen who ran a New York-based investment advisory firm with running a multimillion-dollar scheme built on exactly this door. The court sentenced him to four years in federal prison. The shares he sold to clients were fake. Not undervalued. Not illiquid. Fake. The firm did not own them. There was no special purpose vehicle holding the underlying stock. There was a subscription agreement, a wire instruction, and an account the money went into.

I am being careful here because the public summary available at sentencing did not include every number a reader wants. The name. The firm. The total taken. The count of victims. Those details belong to the docket and will land in the record over time. What the court did adjudicate is the shape of the thing. An adviser. A New York office. Private company shares that were never bought.

That shape is the machine.

III.

Walk through how it works from Edward's chair.

The adviser does not cold call him. That is not how it works at this altitude. Edward gets introduced by a friend from the country club. A real friend. A friend who has been investing with the adviser for two years and just had a great year. The friend is not lying. The friend's statements show gains. Whether the gains are real or whether the friend is being used as the social proof for the next mark is something Edward cannot know from his side of the table.

Edward goes to the office. The office is on a good floor of a good building. There are framed credentials on the wall. There is coffee in a real cup. The adviser is calm, articulate, fluent in the names of the famous private companies. He uses the word access. He uses the word allocation. He says the allocation is small. He says it closes Friday.

Edward goes home. He talks to his wife. He thinks about it for a weekend. This is the part that matters. The mark is not impulsive. The mark is deliberate. The mark does what every financial advice column tells him to do. He thinks about it.

On Monday he wires.

Read that slowly. The fraud did not work because Edward was reckless. The fraud worked because the room was built so that careful people would walk into it and feel careful walking in.

IV.

The concealment was paper. That is almost always what the concealment is.

When the wire clears, the adviser sends a PDF. Confidential Subscription Agreement. The famous name at the top. A share count. A purchase price per share. A countersignature. It looks exactly like what a real private placement document looks like, because real private placement documents are not that complicated. They are a few pages. They are signed. They are filed in a drawer.

Quarterly, Edward gets a statement. The statement shows his position. The position is valued at the last known funding round price. Sometimes the value goes up because the famous company raised at a higher valuation and the news made the paper. Edward sees the number on his statement go up and feels what he is supposed to feel.

He feels smart.

The machine runs on that feeling for as long as the famous company stays private. Years, in some cases. The adviser does not have to perform. He only has to keep sending PDFs.

V.

The structure becomes visible exactly one way. Someone tries to confirm.

A client wants to sell. Or a client's accountant asks for a custodial statement from the entity that actually holds the shares. Or the famous company finally goes public and the client expects his shares to land in his brokerage account on the day of the IPO and they do not.

The client calls the famous company's transfer agent. The transfer agent is the firm that keeps the official list of who owns what. The transfer agent looks up the client's name. The transfer agent says, we have no record of this person. We have no record of this special purpose vehicle. We have no record of these shares.

That is the call where the floor moves.

For Edward, in the version of this story the record supports, the call is short. He calls the famous company. He gets routed. He spells his name twice. The voice on the other end is polite and unhurried. There is no record. He hangs up. He sits at his desk. The folder is open in front of him. The brass pull is on the floor where he set it.

He has done nothing wrong. He has signed documents that meant nothing. He has wired money to an account that was not what it said it was. The adviser is still answering his phone, for now, with the same calm voice, with an explanation about clearing delays and custodial transitions.

The explanation is the last piece of paper in the folder.

VI.

This piece is short because the record is short. A four-year federal sentence. An Italian citizen. A New York advisory firm. Fake shares. The shape of the thing is the lesson, and the shape is older than the defendant.

The private-shares pitch has been around since there were private companies people had heard of. It surges in years when famous startups stay private longer. It surges when retail investors read about IPO millionaires and start asking their advisers if there is a way in. The honest answer, almost always, is no. There are legitimate pre-IPO funds, and they are gated, audited, and slow. The fraudulent version mimics the legitimate version exactly because the legitimate version is what the customer is asking for.

The renaming is this. What the adviser sold was not shares. It was the feeling of owning shares. The PDF was the product. The quarterly statement was the product. The framed credentials and the good coffee and the small allocation closing Friday were the product. The actual equity in the actual company never existed in any account anyone could verify.

Four years is what the court gave him. Edward's folder is still in the drawer.

The brass pull still sticks in summer.

- Law360 | June 2026 | "Investment Adviser Gets 4 Years For Fake Shares Sales" (source article excerpt)

- DOJ / SDNY press releases on prior private-shares advisory fraud cases (pattern context)

- SEC enforcement actions on fraudulent private placement and SPV schemes (pattern context)

- Egan, Matvos, Seru, "The Market for Financial Adviser Misconduct," Journal of Political Economy (industry context on adviser misconduct rates)

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.