The mayor sold the house to his business partner and stayed in it

Nathaniel Anderson sold his foreclosed Willingboro home to a business associate, swore he would leave, and stayed. A federal jury saw through it. On June 1, a judge sent him to prison.

The house did not move.

That is the part that matters. The deed changed hands in October 2015. The mortgage on it was discharged by a government-sponsored lender that took a loss of more than two hundred thousand dollars. A new mortgage was written for one hundred sixty-two thousand and change. The buyer signed a sworn document saying she would live there as her primary residence. The seller signed a sworn document saying he would vacate.

The seller did not vacate. The buyer did not move in. The house, on the inside, was the same house with the same man in it.

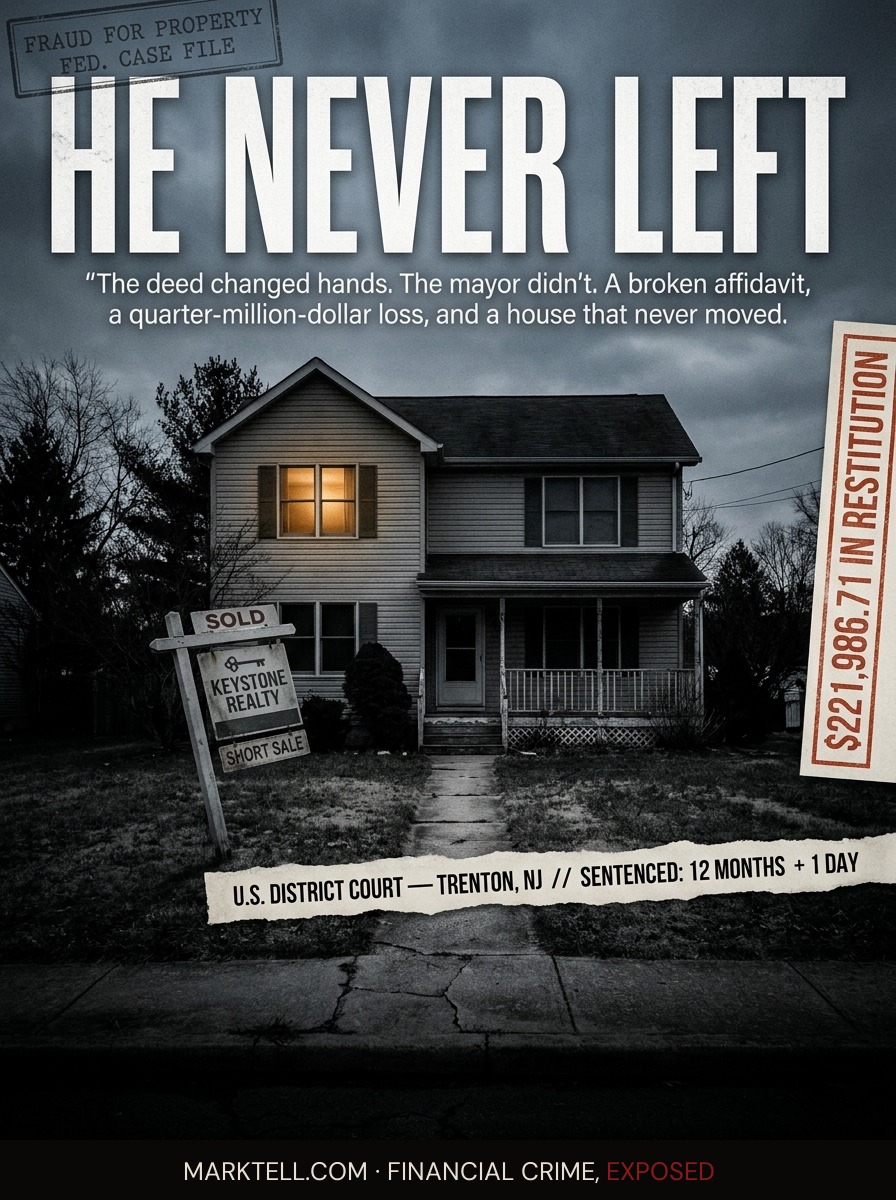

The man was Nathaniel Anderson. He was the mayor of Willingboro Township at one point. He was still a councilman when the federal indictment came down. On Monday, June 1, 2026, he stood in front of U.S. District Court Judge Robert Kirsch in Trenton and was sentenced to twelve months and one day in federal prison.

The "and one day" is not a flourish. It is a legal trigger that makes a sentence eligible for good-conduct credit. The federal system is full of details like that. The whole case, in the end, was about details like that.

I.

Marlene is 62. She works for the federal government in a building in suburban Maryland and has for thirty-one years. She does not know Nathaniel Anderson. She has never been to Willingboro. Her pension is partly invested, the way many federal pensions are, in the same government-sponsored mortgage enterprises that ended up holding the bag on his house.

When you ask who got hurt in a case like this, the honest answer is that the harm was diffuse. It did not land on one person's kitchen table. It landed on a balance sheet at a quasi-governmental lender, and that balance sheet is held up, in the end, by people like Marlene and by the taxpayers who stand behind the enterprise when its losses get big enough.

That is the part that gets lost when these cases get reported. The fraud is described as a fraud against a "lender," as if a lender were a building. The lender is a pool of money. The pool of money belongs to people. Marlene is one of them.

She will never read the indictment. She will never know the case number. She will absorb her small share of the loss in the way pension holders always do, which is to say invisibly, across decades, in the form of slightly worse returns than she would have had if the man in Willingboro had moved out of his house when he said he would.

II.

Here is what a short sale is, in the plainest terms.

A homeowner owes more on the mortgage than the house is worth. Or the homeowner cannot pay. The lender, rather than foreclose and resell, agrees to let the homeowner sell the house for less than the loan balance. The lender takes the loss. The homeowner walks away. The buyer gets the house at the reduced price.

The whole structure depends on two things being true. First, the sale has to be arm's-length, which is the legal term for "between strangers who do not have a side deal." Second, the seller has to actually leave. If the seller stays, the lender has just been tricked into forgiving a debt for a homeowner who kept the house. That is not a short sale. That is a gift, taken by deception.

In the Willingboro case, both pillars were false.

According to the U.S. Attorney's office and the trial record, Nathaniel Anderson and Chrisone Anderson, the buyer, had a prior business relationship. The mortgage application stated they did not. Nathaniel Anderson signed paperwork saying he would vacate the property. He did not. Chrisone Anderson signed paperwork saying she would occupy it as her primary residence. She did not.

The lender, believing all four of those things were true, discharged the original mortgage. The original loan had been roughly $350,000. The new loan to Chrisone Anderson was $162,011. The gap is the loss.

The restitution number entered by the court is $221,986.71. That figure includes the loss plus the carrying costs and fees the lender absorbed.

III.

Read the chronology.

March 2015. The conspiracy begins.

October 2015. The foreclosure happens. Same day, on the same desk, the sales contract to Chrisone Anderson is executed. One signature ends the old loan. Another signature starts the new one. The house in between does not move.

June 2017. The scheme ends.

August 22, 2024. A federal grand jury indicts both defendants.

Early 2026. Two-week trial. Jury convicts.

June 1, 2026. Sentencing in Trenton. Nathaniel Anderson: 12 months and one day. Chrisone Anderson: 8 months of home confinement. Three years of supervised release each. Joint restitution of $221,986.71.

Eleven years from the start of the fraud to the sentencing. That is not unusual for these cases. Mortgage fraud lives in the paperwork. The paperwork is dull. The paperwork has to be read by someone who knows what they are looking for, and then it has to be assembled, and then it has to be presented to a grand jury, and then a defendant has the right to trial, and trials take time.

Eleven years. The man stayed in the house through most of them.

IV.

What does the machine look like, stripped down.

A homeowner is underwater. He does not want to lose the house. He does not have the cash to catch up the mortgage. He cannot qualify for a refinance, because his credit and his income do not support the existing loan.

So he finds a partner. The partner buys the house at a discount using the short sale process. The lender, told that this is a transaction between strangers, agrees to take the loss. The partner takes out a new, smaller mortgage. The original homeowner stays in the house. He pays the partner rent or mortgage payments, or perhaps he pays nothing at all and the partner handles it as part of their existing business arrangement.

On paper, the house changed hands. In life, nothing changed.

The lender has been used. The original debt has been forgiven for a borrower who did not need forgiveness in the sense the program was designed to provide. He needed a financial restructuring, and he got one, and he used a fraud to get it.

This is what federal prosecutors call a "fraud for property" scheme. It is one of the most common forms of mortgage fraud and one of the hardest to detect, because every single document looks normal. The signatures are real. The notarizations are real. The new loan really is a loan to the named buyer. The only thing that is false is the relationship between the two people on the contract and the question of who is going to live in the house.

V.

The arm's-length affidavit is one page. Sometimes two. It is signed by both the buyer and the seller. It states, under penalty of perjury, that the parties are not related by blood, marriage, or business, and that there is no agreement between them, written or oral, allowing the seller to remain in the property or to repurchase it.

That single page is the lock on the door of the short sale program. Without it, the program does not work. The lender has no other way to know whether the people on the contract are strangers. There is no national database of business relationships. There is no inspector who shows up to verify that the buyer's furniture has been moved in. The whole thing runs on the affidavit.

When the affidavit is false, the lock is broken. The program operates as designed but on false inputs, and the loss goes out the door before anyone notices.

This is what the federal jury in Trenton found beyond a reasonable doubt. The lock was broken on purpose. The signatures were the tools.

VI.

Marlene, the federal employee whose pension is part of the pool, will never see a refund. The restitution order is real and the defendants are jointly obligated for $221,986.71, but restitution in fraud cases is collected slowly, when it is collected at all. The defendants will pay what they can, on a schedule the court will set, and the rest will be absorbed.

That part may be the closest thing to a moral in this story. The loss has already happened. The conviction does not return the money. The conviction announces, in public, that the lock was broken and that the people who broke it were caught. The next person considering the same scheme reads about the sentence and decides whether twelve months in federal custody is a price they are willing to pay.

Some will decide yes. Some will decide no. The deterrent works the way deterrents work, which is imperfectly and over time.

VII.

Chrisone Anderson's attorney, Troy A. Archie, has said he intends to appeal the conviction to the Third Circuit Court of Appeals. Allegation is not adjudication on the appellate questions, and the appellate process will run its course.

For now, the trial record stands. Two defendants. One house. One lender. One arm's-length affidavit that was not arm's-length.

The man stayed in the house.

That is the case. That is the whole case. Strip every legal term out of it and that is what the jury saw. He signed a paper saying he would leave. He did not leave. The lender forgave a debt because it believed he would leave. The lender was wrong, because he had told it a thing that was not true.

Twelve months and one day. The day matters because of the credit. The day always matters. The whole case was about the days, and the signatures on the days, and the house that did not move while the papers around it did.

VIII.

If you are reading this because you are underwater on a mortgage and someone has suggested a friend could buy the house and let you stay, here is what the Willingboro case tells you. The friend is not your friend in the eyes of the law. The friend is your co-defendant. The arm's-length affidavit is not a formality. It is the document the federal government will use to put you in front of a judge.

Eleven years from the start of this scheme to the sentence. The federal government does not forget. It moves slowly. It moves anyway.

The house was the same house the whole time. That was the problem. That was always going to be the problem.

- U.S. Attorney's Office, District of New Jersey | June 1, 2026 | Sentencing announcement, United States v. Nathaniel Anderson and Chrisone Anderson

- Federal grand jury indictment | August 22, 2024 | District of New Jersey

- News12 New Jersey | June 2026 | "Former Willingboro Mayor Sentenced To Federal Prison For Short Sale Mortgage Fraud"

- FBI Newark Division, Trenton Resident Agency | Investigation record

- Federal Housing Finance Agency, Office of the Inspector General, Northeast Region | Investigation record

- U.S. District Court for the District of New Jersey | Judge Robert Kirsch, sentencing hearing, June 1, 2026, Trenton

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.