The letters said the money was safe. The money was already gone.

Bob Hunter ran a Springfield retirement shop called The Summit Group of Missouri. For years, his clients got statements showing their money was right where it should be. On June 11, he pleaded guilty to wire fraud and money laundering. The statements were the crime.

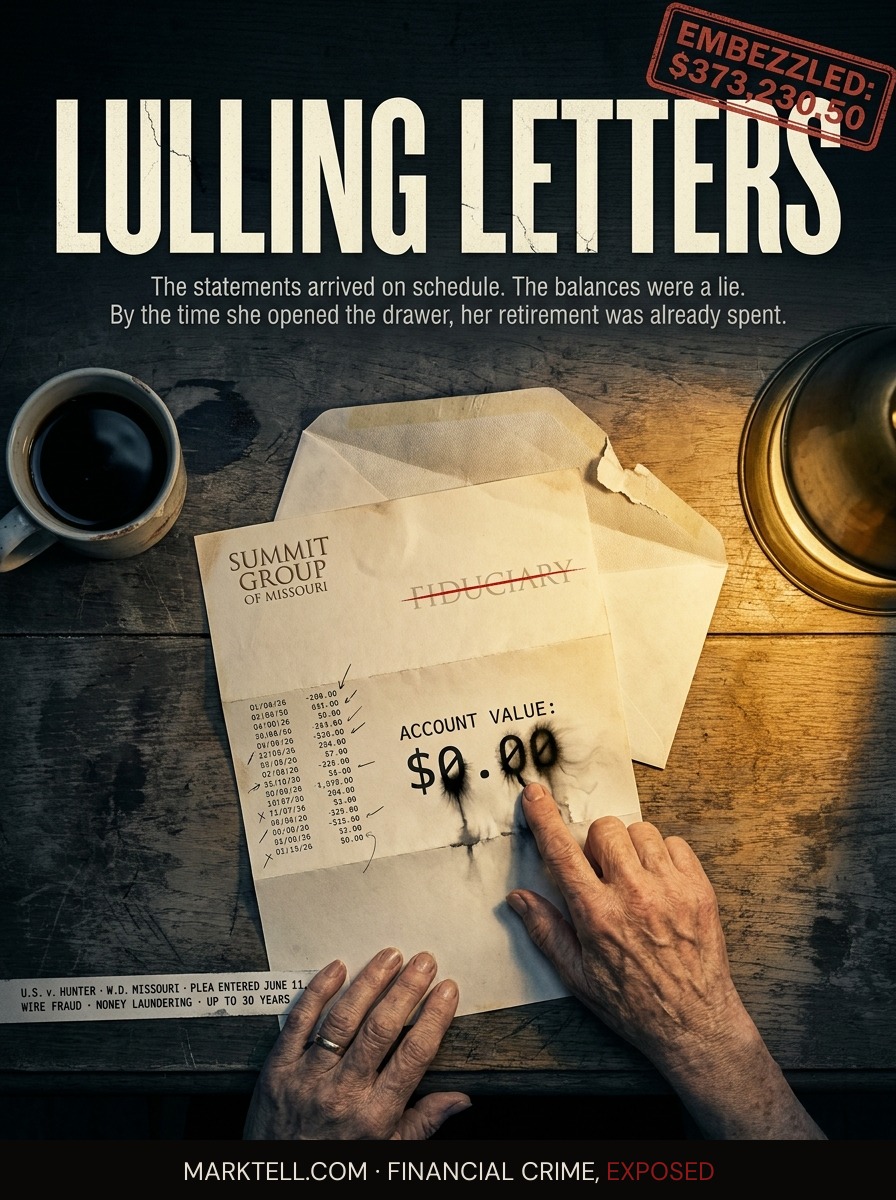

Linda sat at the kitchen table on a Sunday afternoon in Springfield with the envelope in front of her. Summit Group of Missouri. She knew the logo. She had been getting envelopes like this one for years.

She was sixty-eight. She had run the billing office at the hospital for almost three decades before she retired. She knew how to read a statement. She ran her thumb down the column the way she used to run it down a patient account, looking for the line that did not match.

The line matched. The balance was where it should be. A little higher than last quarter, even. She folded the statement in thirds and put it in the drawer where she kept the other ones.

The money in that drawer did not exist.

That is the thing you have to sit with for a minute. The statements were real. The paper was real. The logo was real. The number printed under the words ACCOUNT VALUE was not real. It had not been real for a long time.

Bob Hunter pleaded guilty on Wednesday, June 11, 2026, in front of U.S. Magistrate Judge David P. Rush. He is seventy-two. He ran The Summit Group of Missouri Inc. and a thing called the Master Trust under The Summit Group of Missouri. He sold what are called Supplemental Executive Retirement Plans. A SERP, in plain English, is a retirement account a company sets up for an executive on top of their regular 401(k). It is supposed to sit there and grow. Hunter was the man who administered them.

He admitted he stole $373,230.50 from clients who thought their money was being invested.

He admitted the statements were the cover.

I.

In the trade, the fake statement has a name. The DOJ calls it a lulling letter. It is exactly what it sounds like. A letter that lulls. A piece of paper that arrives on a schedule, looks like the last one, says the money is still there, and buys the operator another quarter before anyone asks a question.

I have seen this technique from the inside. Not Hunter's office. Other rooms. The lulling letter is older than the wire transfer. It worked in the bucket shops in the twenties. It worked in the boiler rooms in the eighties. It works now because it is built on the one thing the mark wants more than the truth.

The mark wants to not have to look.

If the statement arrives and the number is bigger than last time, the mark does not call. The mark files it. The mark goes back to Sunday afternoon. The lulling letter is the lock on the door. It is the thing that keeps the door closed while the room behind it empties out.

Hunter's clients got the letters. The letters showed money that was not there. According to the DOJ release surrounding the plea, the false reports were used to conceal the nature and scope of the embezzlement and to delay detection. That is the prosecutor's language. In the room, it is simpler. The letters were the crime. The wire transfer was just how he got paid.

II.

Picture Linda again. She did not roll her SERP into Summit because she saw an ad. She did it because Bob Hunter was a man she had seen at church. He had been doing this in Springfield for years. He had a small office with framed certifications on the wall. He used the word fiduciary, which means a person legally required to put your interests ahead of his own. He used the word trust, which has two meanings in finance and he was happy to let both of them blur.

She signed the rollover form. The form moved her money into Summit. The money she had been setting aside in the SERP at the hospital for the back half of her career.

That signature was the hour-five signature. Not because anyone pressured her at the table. Because by the time the pen was uncapped, the relationship had already done all the work. She trusted him. The form was just paperwork.

The money left her old account and went into the Master Trust.

The Master Trust is where the lock turned.

III.

Here is the simple version of what the plea says happened next.

The money was supposed to be invested in the SERPs Hunter promoted and administered.

The money was used for personal expenses.

That is the betrayal in one sentence. The rest is mechanics.

The mechanics are these. The statements kept printing. The statements kept arriving. The statements showed balances that had been spent. The IRS Criminal Investigation division and the FBI eventually walked the paper backward, from the statement to the trust account to the wire to the personal expense. That is how these cases are made. Not by genius. By patience. By an agent sitting at a desk with bank records and an envelope from Linda's drawer.

The total in the plea is $373,230.50. Read that number slowly. It is not the kind of number that makes a national headline. It is the kind of number that empties three or four retirements. It is enough to take a woman who planned to spend Decembers with her grandkids and put her back behind a desk at sixty-nine.

That part may be the saddest. The number is small enough that it almost did not get written about. The people it took it from are not small.

IV.

The plea was entered in the Western District of Missouri. Assistant U.S. Attorney Patrick Carney is prosecuting, under U.S. Attorney R. Matthew Price. Hunter faces up to twenty years on the wire fraud count and up to ten on the money laundering count, with maximum fines of $250,000 on each. Sentencing comes after a presentence investigation. He has not been sentenced yet. He may never serve the maximum. Almost no one does.

The DOJ tied the case to its new National Fraud Enforcement Division, announced April 7, 2026, and to the Task Force to Eliminate Fraud. In the same district, three weeks earlier, an Illinois man named Syed M. Makki was sentenced to 15½ years for an elder fraud conspiracy where victims liquidated savings and retirement accounts to buy gold bars. Restitution in that case was set at $4,754,000.

Different machine. Same fuel. Retirement accounts belonging to people who had stopped earning new money.

V.

I want to go back to the kitchen.

Linda is not Linda. She is a composite built from the kind of client The Summit Group of Missouri had. The kitchen table is a kitchen table somewhere in Greene County, Missouri. The statement in the drawer is a real document type. The DOJ confirmed in its release that clients received false investment reports claiming money existed in their accounts when it did not.

I do not know the day Linda's real-life equivalent found out. I know how this usually goes. There is a moment. A request for a withdrawal that gets a slow answer. A phone call that goes to voicemail twice in a week. A letter from a federal agency. The drawer gets opened. The statements come out. The folded paper that said the money was safe gets read again under a different light. The number on the page does not change. What changes is the person reading it.

That is the moment the lulling letter stops working. It is also the moment the mark realizes that the letter was never really a statement. It was a sedative. It was something the operator sent so the client would not call.

VI.

If you are reading this because you are trying to protect someone, here is the ugly version of what to look for. Not the exciting questions. The ugly ones.

Who actually holds the money. Not the advisor. The custodian. The bank or trust company whose name is on the statement. If the statement comes from a company the advisor controls, you do not have a statement. You have a letter.

Whether the advisor can move money without a second signature. If one person can wire client funds without a custodian or co-signer in the loop, the lock is already open.

Whether anyone audits the trust. A trust with no outside audit is a room with no window.

Whether the statements ever go down. Real investments go down sometimes. Lulling letters almost never do.

And the one that hurts. Whether you picked this person because of the math or because of the relationship. The church. The Rotary. The referral from a friend. The relationship is not the disqualifier. The relationship is the warning to look harder at the math, not less.

Bob Hunter has admitted what he did. The Western District of Missouri has his plea. A judge will set a sentence. Somewhere in Springfield, an envelope is sitting in a drawer with a number printed on it that does not exist.

That is not a statement. That was never a statement.

The statement was the lock.

- U.S. Attorney's Office, Western District of Missouri | June 11, 2026 | DOJ press release on guilty plea of Bob Hunter

- Springfield News-Leader | June 11-12, 2026 | "Springfield man pleads guilty to embezzling clients' retirement funds"

- U.S. Department of Justice | April 7, 2026 | Announcement of National Fraud Enforcement Division

- U.S. Attorney's Office, Western District of Missouri | May 21, 2026 | Sentencing of Syed M. Makki, elder fraud conspiracy

- Federal statutes | 18 U.S.C. § 1343 (wire fraud), 18 U.S.C. § 1957 (money laundering) | statutory maximums cited

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.