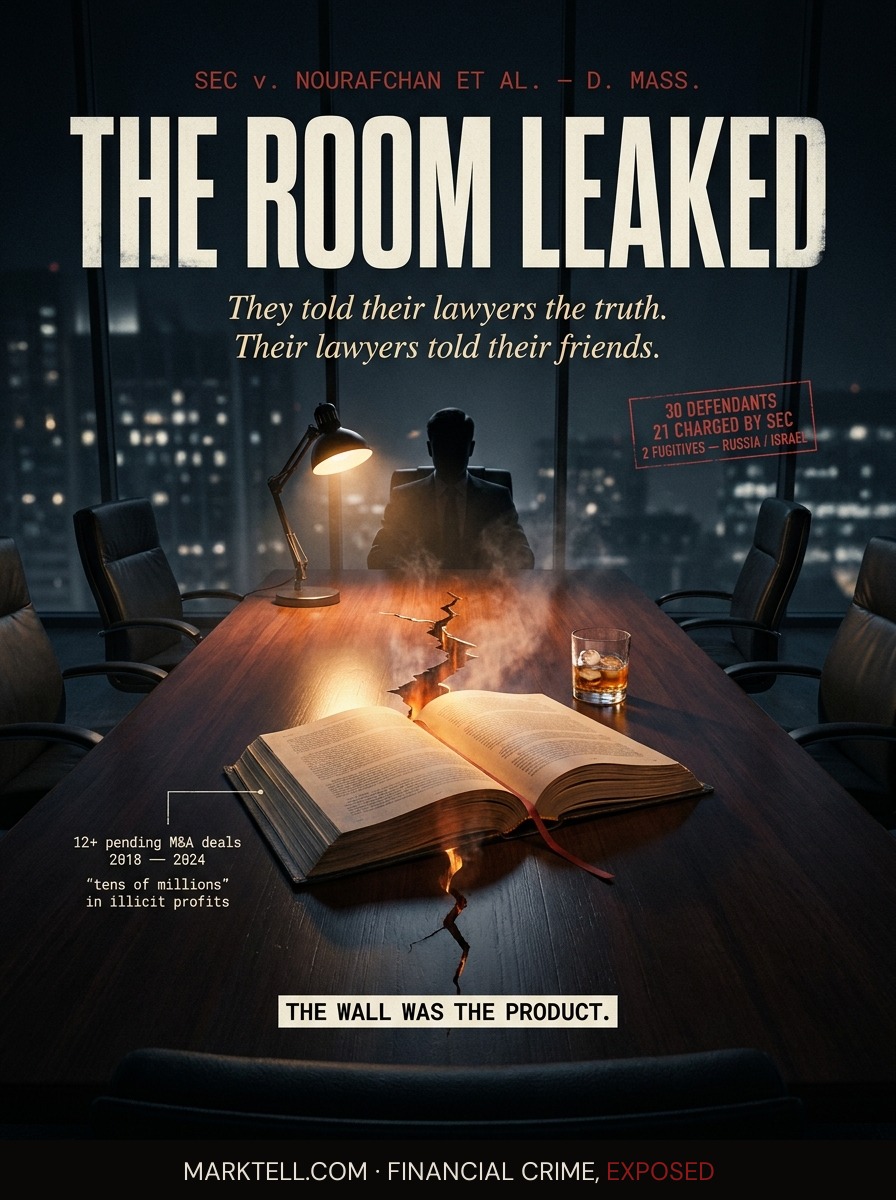

The lawyer at the conference table knew the deal before the market did. So did his friends.

The SEC says a Los Angeles M&A attorney and a Long Island trader ran a leak pipeline out of global law firms for six years, turning client confidences into trades. Twenty-one defendants. Twelve-plus deals. Two fugitives.

The associate is still in the office at 9:14 p.m. on a weekday. The cleaning crew has come and gone. The binder is open on the conference table. Inside the binder is everything: the buyer, the seller, the price per share, the announcement window, the names of the bankers, the carve-outs, the regulatory risk paragraph the partners have been arguing about for a week.

This is privileged. The client told the firm because the client had to tell someone. That is what attorney-client privilege is for. You hire a lawyer and you hand them the truth and the law agrees that the truth stays in the room.

The room is the product the client is buying.

According to the complaint the Securities and Exchange Commission filed this morning in federal court in Massachusetts, the room had a leak. More than one. For six years.

The SEC says twenty-one people participated in a scheme that ran from 2018 through 2024, fed by material nonpublic information taken from multiple global law firms, used to trade ahead of more than twelve pending corporate transactions, mostly mergers and acquisitions. The agency calls it "millions of dollars in illicit profits." The U.S. Attorney's Office for the District of Massachusetts, charging in parallel today, calls it "tens of millions." The criminal case names thirty defendants. Nineteen are in custody. Two are fugitives, one in Russia, one in Israel.

Read that slowly. Two countries the United States cannot easily reach into.

The SEC names Nicolo Nourafchan, an M&A attorney based in Los Angeles, as the orchestrator. It names Robert Yadgarov of Long Beach, New York, as his partner. It says an additional corporate lawyer was recruited to keep the pipeline filled. The agency does not name the law firms. It does not name the deals. The complaint is precise about the structure and quiet about the addresses.

These are allegations. No one has been convicted. The defendants are entitled to defend themselves and several of them will. That part of the system also works as designed.

What the agency describes is not a tip. A tip is one phone call, one stock, one conscience that breaks once and then breaks again. What the agency describes is infrastructure.

Call it the pipeline.

On one end of the pipeline is a conference table at a law firm with a binder on it. On the other end is a trading screen somewhere with a person watching the open. In between is a network of people whose only job is to keep the information moving and the trades looking ordinary. Different brokerages. Different account names. Different countries. The complaint says the SEC received assistance from regulators in Denmark, the United Kingdom, Cyprus, Mauritius, and Switzerland. Five jurisdictions. That is not a coincidence. That is the route.

This is the part that matters if you are a person who has ever sold a stock or bought one. When you placed that trade, somebody was on the other side. You assumed the other side was guessing the same way you were guessing. You assumed you were both reading the same news.

If the SEC's allegations hold up, on more than twelve specific deals between 2018 and 2024, somebody on the other side of somebody's trade was not guessing. They had the binder.

That is what insider trading actually steals. People talk about it as a victimless crime, a paper offense, the kind of thing where nobody gets hurt because the money was going to move anyway. That framing is wrong. The thing that gets stolen is the premise. The premise that the market is a place where the information is roughly the same on both sides of the line. Once that premise is gone, the people on the slow side are funding the people on the fast side and they do not know it.

Joseph G. Sansone, who runs the SEC's Market Abuse Unit, has said before that his team's edge is data. The unit operates an Analysis and Detection Center that looks for clustering. Trades that hit the same names ahead of the same announcements. Accounts that show up next to each other again and again. The pattern is what gives the scheme away, because the human brain that runs a scheme like this cannot help repeating itself. It finds a thing that works and it does the thing again. By the fifth time, the heat map lights up.

The SEC's complaint, filed in the U.S. District Court for the District of Massachusetts, asks the court for injunctive relief, disgorgement of the profits with prejudgment interest, and civil money penalties. Disgorgement means giving back what you took. Prejudgment interest means giving back what the money would have earned in the meantime. Injunctive relief means a court order telling the defendants not to do this again. The criminal case, brought by the U.S. Attorney's Office, carries the possibility of prison.

There is a piece of this that is going to get lost in the headline count, and it should not. The complaint alleges that lawyers did this. Not IT contractors. Not paralegals. Not cleaning staff who happened to read a binder. Lawyers, including a practicing M&A attorney, are alleged to have used the information their clients trusted them to hold.

The client hires the firm because the firm is supposed to be the wall. The wall is what the client is paying for.

If the allegations are true, the wall had a door cut into it, and the door had been there for years, and the people walking through it were the people the wall was made of.

The defendants will respond in court. Some will fight. Some may plead. Two are abroad and may never sit at a defense table in Boston. The case will move on the schedule federal cases move on, which is to say slowly, and the next round of filings will be technical, and the headlines will fade, and somewhere in a global law firm tonight there is another associate pulling another binder for another deal, and the wall is still the product.

The pipeline does not need every law firm. It only needs one room with a door.

That is the part the next case will turn on.

- SEC Press Release | May 6, 2026 | "SEC Charges 21 Individuals with Alleged Wide-Reaching Insider Trading Scheme" | https://www.sec.gov/newsroom/press-releases/2026-44-sec-charges-21-individuals-alleged-wide-reaching-insider-trading-scheme

- SEC Complaint | May 6, 2026 | U.S. District Court for the District of Massachusetts (referenced in SEC release)

- U.S. Attorney's Office, District of Massachusetts | May 6, 2026 | Parallel criminal charges (referenced in SEC release and research brief)

- SEC Division of Enforcement | Market Abuse Unit / Analysis and Detection Center (program references)

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.