The invoices were for trucks that never moved. The Lamborghini was real.

A federal indictment unsealed in Chicago accuses an Orland Park freight company owner of billing for shipments that never happened and inflating bakery franchises before selling them. The receipts are parked in his garage.

Daniel sat at his kitchen table on a Sunday in the fall and read the prospectus for the third time. He was fifty-two. He had spent twenty-six years as an operations manager at a regional logistics company and he had been laid off in the spring. He had a wife who taught third grade and a daughter starting at a state school. He had a 401(k) he did not want to drain and an SBA loan he had been pre-approved for and a folder on the kitchen table with a yellow highlighter on top of it.

The folder was about a bakery franchise. Two locations. Steady revenue, the broker had said. Owner wants to retire. Books are clean.

The numbers in the folder told a story Daniel wanted to be true. Monthly revenue. Cost of goods. A line for owner's discretionary earnings that, if you squinted, looked like a livable income. He highlighted the revenue line. He highlighted the customer count. He went to the location on a Tuesday morning and watched people come in and order coffee and a kolache and he counted the transactions in his head.

He did not know that the numbers in the folder were not the numbers in the register. The federal indictment unsealed on May 7, 2026 in U.S. District Court in Chicago alleges that the man selling the franchise had inflated the value of the bakery franchises before selling them to an unsuspecting buyer. That is the language in the charging document. An unsuspecting buyer.

Daniel is a composite. The buyer in the indictment is real.

I.

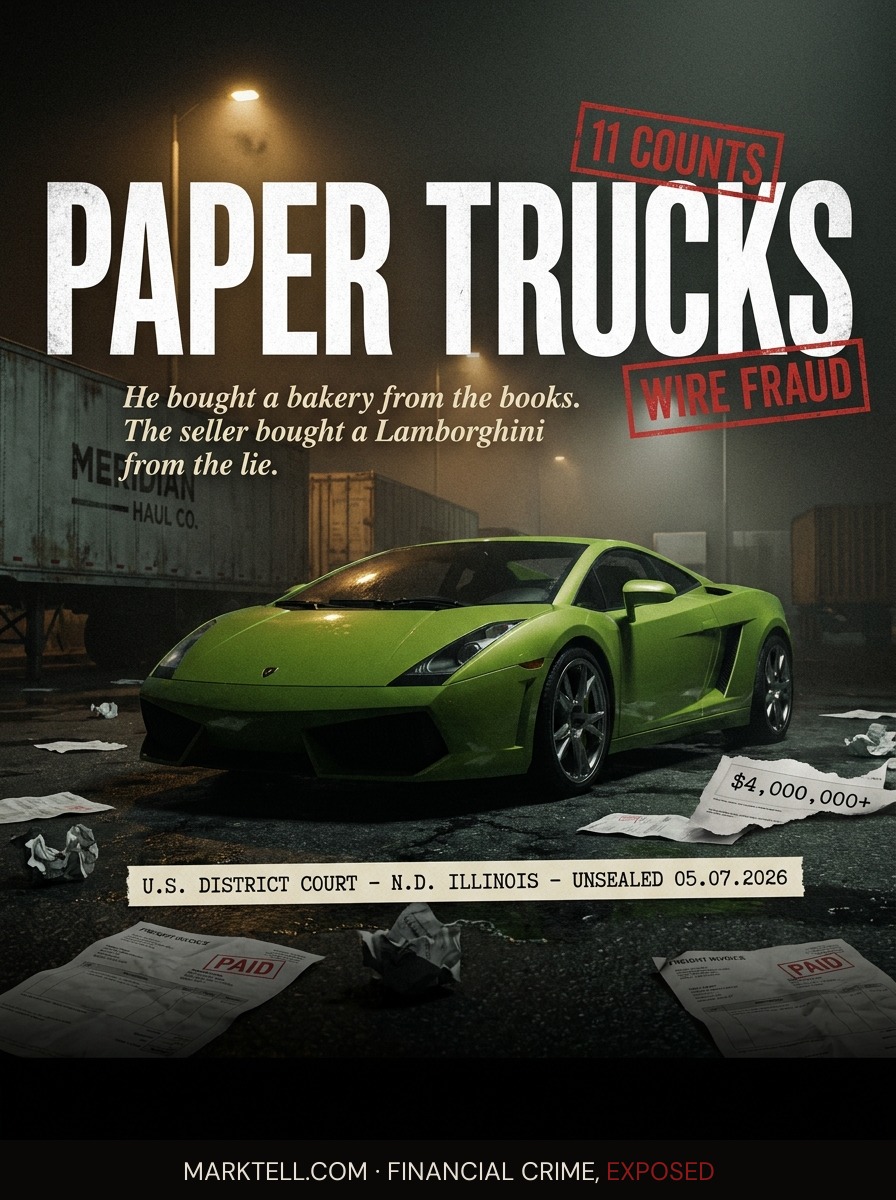

The man named in the indictment is Raed Naser, 41, of Crown Point, Indiana. He owns a freight transport company in Orland Park, the kind of business that lives in an industrial park off an Illinois interstate, with a small office and a yard for trailers and a phone that rings when something needs to be moved from one warehouse to another.

That is the company on the letterhead. The company that, the indictment alleges, sent invoices for freight shipments that never happened.

Read that slowly. The trucks did not roll. The cargo did not load. The miles were not driven. But the invoice went out, and the invoice got paid, and the money landed in an account Naser controlled.

Eleven counts of wire fraud. Four counts of money laundering. Total alleged take: more than $4 million across two schemes. The U.S. Attorney's Office for the Northern District of Illinois announced the charges. Andrew S. Boutros is the U.S. Attorney. Heidi Manschreck is the Assistant U.S. Attorney handling the case. The FBI's Chicago Field Office and the U.S. Postal Inspection Service investigated. Naser pleaded not guilty before U.S. Magistrate Judge M. David Weisman. A status hearing is set for June 10, 2026 at 9:45 a.m. before U.S. District Judge Sharon Johnson Coleman.

Allegation is not adjudication. Naser is presumed innocent. Those are the rules of the room.

Inside the rules, the indictment lays out a machine.

II.

Call it the paper truck.

A real freight company has trucks and drivers and dispatchers and fuel cards and bills of lading. A bill of lading is the document that proves cargo moved from point A to point B. It is the receipt of the road. The federal allegation is that Naser's company generated invoices without the road. Paperwork for movement that did not occur. A trucking business on the surface, a billing operation underneath.

The thing about a paper truck is that it never breaks down. It never gets pulled over. It never has to refuel. It only has to be believable enough that the customer who receives the invoice pays it without checking the underlying movement. In a freight relationship with high volume and tight margins, that is easier than it sounds. Invoices stack up. Accounting departments cut checks against purchase orders. Nobody has time to walk a load from origin to destination on every line item.

That is one half of the indictment. The freight half.

The other half is the bakery half, and the bakery half is where Daniel sits.

III.

The indictment alleges that Naser fraudulently inflated the value of bakery franchises before selling them to an unsuspecting buyer. The federal prosecutors did not use the plural "buyers." They used the singular. One buyer. Someone like Daniel, but not Daniel. A real person who put real money into something that had been dressed up to look like more than it was.

Inflating the value of a small business is its own kind of paperwork. You can do it by overstating revenue. You can do it by understating expenses. You can do it by booking sales that did not happen, the way the freight side allegedly booked shipments that did not happen. Numbers, on a page, in a folder, on a kitchen table.

The buyer reads the folder. The buyer borrows against the folder. The buyer signs at the closing table.

Then the buyer takes over the business and finds out the folder and the register do not match.

That is the moment Daniel does not get in this story because Daniel is a composite. But the buyer in the indictment got it. Some morning. Some Monday. Some look at the bank deposit report against the projection in the prospectus, and the gap.

IV.

The proceeds, the indictment alleges, did not stay in the business accounts. They moved.

A Lamborghini Huracan. A BMW M8 Gran Coupe. A Cadillac Escalade.

Those are not investments. Those are not assets that throw off cash flow. Those are the things you buy when the money has come in faster than you can explain it and you want it to become something solid before anyone asks where it came from. A Lamborghini in a driveway is the loudest receipt in financial crime. It says: I had it, I spent it, the money was here.

That is also why prosecutors love it. Vehicles have titles. Titles have dates. Dates can be lined up against deposits, and deposits can be lined up against invoices, and invoices can be lined up against the cargo that never moved.

The trail does not evaporate. It parks in the garage.

V.

Daniel, the composite, would not have known about the Lamborghini when he signed. He would have known about the broker's smile and the spreadsheet's clean lines and the morning he stood inside the bakery and counted customers. He would have signed because the math, as presented, said this was a business that could feed a family and pay back a loan.

He would have learned about the Lamborghini the way the public learned about it. From a press release. From a news article on a Saturday morning. From a federal court file unsealed on a Wednesday in May.

That is the gap this column exists to close. The gap between what the buyer saw at the closing table and what the buyer learns from a court filing two years later. The folder on the kitchen table did not say "the seller will use your loan proceeds to buy a Lamborghini." The folder said: monthly revenue, cost of goods, owner's discretionary earnings.

The folder was the stage. The cars are the receipts.

VI.

If you are reading this because you already bought a small business and the numbers in the folder do not match the numbers in the register, here is what the record in this case suggests about where to look.

Pull the bills of lading or their equivalent. In a freight context, that means the actual movement records. In a bakery context, it means the daily Z-tapes from the register, the supplier invoices for flour and sugar and packaging, the payroll runs, the merchant processor statements. Real businesses leave real residue. The residue is harder to fake than a summary spreadsheet because it has to match itself across multiple unrelated systems.

Compare what the seller showed you to what the underlying systems say. If the prospectus claimed $X in monthly revenue and the merchant processor shows materially less, that is not a discrepancy. That is a fingerprint.

Talk to a forensic accountant before you talk to a lawyer. The lawyer will ask what the damages are. The accountant will tell you.

And keep the folder. The folder is evidence. The yellow highlighter is evidence. The email chain with the broker is evidence. Whatever made you sign is what a prosecutor or a civil attorney will use to show the gap between what was promised and what was delivered.

VII.

The case against Naser is at the beginning. He has pleaded not guilty. The status hearing is in June. A trial, if there is one, is months away. The cars, if the government can establish what the indictment alleges, will likely be subject to forfeiture. The buyer of the bakery franchise will pursue restitution and may collect a fraction of what was lost on a timeline measured in years.

That is the part of these cases nobody puts in the press release.

The indictment is the loud day. The day the FBI and the Postal Inspectors finish what they started and the U.S. Attorney's Office stands at a microphone and lists the cars. The quiet days are the ones the buyer lives through afterward. The conversation with the spouse. The conversation with the loan officer. The decision about whether to keep the bakery open or close it. The folder on the kitchen table, the same folder, read again with a different eye.

Daniel is a composite. The buyer is real. The Lamborghini is real. The trucks were not.

The freight never moved. Only the money did.

- U.S. Attorney's Office, Northern District of Illinois | May 7, 2026 | Press release announcing indictment of Raed Naser

- U.S. District Court, Northern District of Illinois | May 7, 2026 | Indictment unsealed, 11 counts wire fraud, 4 counts money laundering

- Patch | May 9, 2026 | "Owner Of Orland Company Indicted On $4M In Fraud Used Money To Buy Lambourghini, Escalade: US Attorney"

- Federal Reserve Board, Vice Chair Bowman remarks on consumer fraud | May 5, 2026 | Speech on financial fraud risks

- 2025 Survey of Household Economics and Decision Making | 2025 | Federal Reserve survey on financial fraud incidence

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.