The IPO opened at six dollars. The phone said it was going to forty.

A federal lawsuit alleges social media operators ran coordinated pump-and-dumps through tiny Nasdaq IPOs, several lead-underwritten by Fort Washington's Bancroft Capital. The filing asks the question every retail investor should: hapless victim, or greedy enabler.

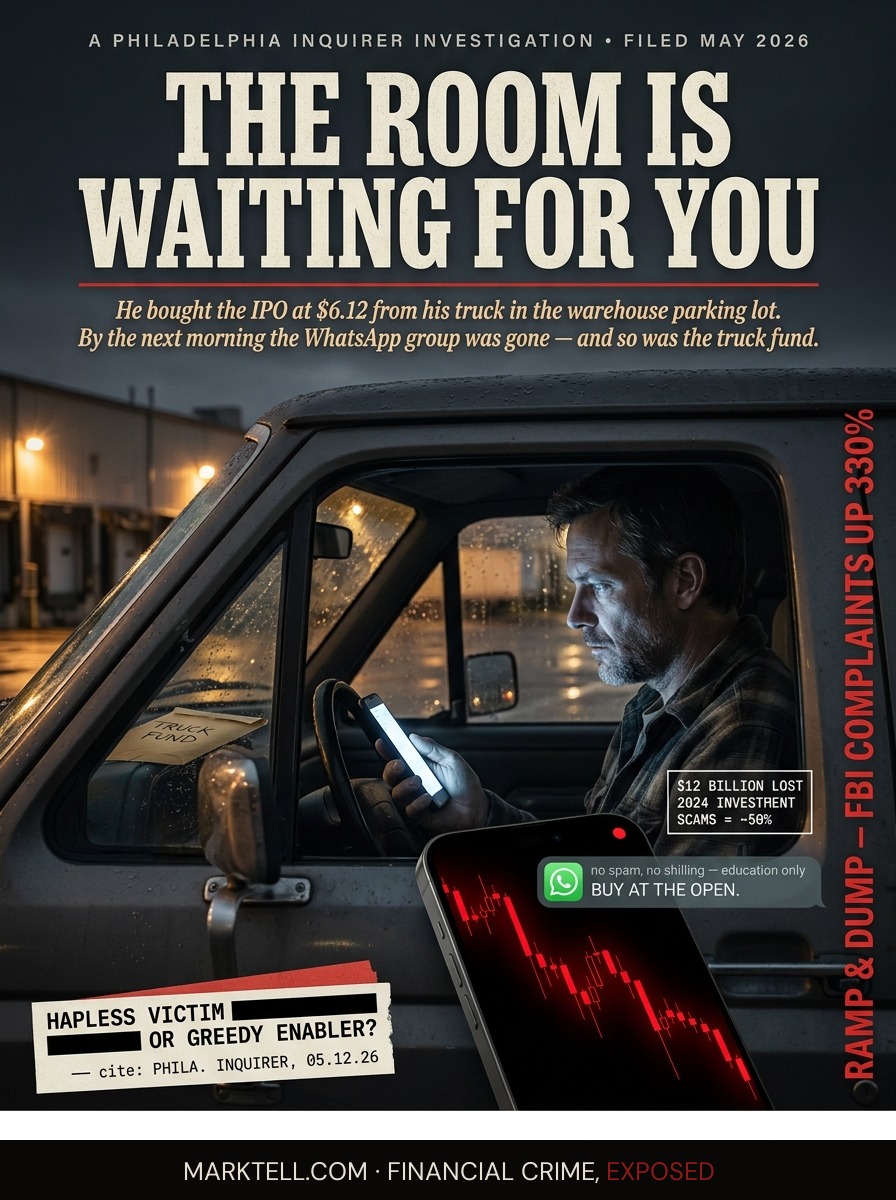

Marcus was forty-seven years old and ran the second shift at a logistics warehouse outside Allentown. He had a wife, two kids in middle school, and a 2014 F-150 with 188,000 miles on it that he was trying to replace. He kept a savings envelope in the top drawer of the dresser. He called it the truck fund. By April of 2025 it had a little over nine thousand dollars in it.

The Facebook ad showed an older man in a navy suit standing in front of a chart. Free training. A link to a Telegram channel. The Telegram channel pointed to a WhatsApp group. The WhatsApp group had four hundred and some members and a pinned message that said "no spam, no shilling, education only." The man who ran it called himself an analyst. He posted screenshots of his brokerage account. The numbers were big and they were green.

Marcus lurked for three weeks. He watched the group call two small stocks before they ran. He missed both. He told himself he would not miss the next one.

The next one was an IPO. A tiny Nasdaq listing. Six dollars at the open. The group had been talking about it for ten days. The analyst said it was going to forty. He said the float was small, which was true. He said the company had partnerships in Asia, which was harder to verify. He said the IPO day was the only entry point. He said it three times in three different ways.

Marcus put in the buy order at 9:28 AM from the parking lot of the warehouse, sitting in the truck he was trying to replace. He bought at six-twelve. By 11:47 the stock was at eighteen. He took a screenshot. He thought about texting his wife. He did not. He wanted to surprise her.

By 3:54 PM the stock was at five-eighty. By the close the next day it was under three.

The WhatsApp group went quiet. Then the group was deleted. Then the analyst's Telegram channel was deleted. Marcus refreshed his brokerage app at the kitchen counter that night while his wife was upstairs and watched the position sit there like a body no one had come to claim.

He had been the buyer the room was waiting for.

This is the room.

According to reporting by the Philadelphia Inquirer published May 12, 2026, a federal lawsuit alleges that social media operators ran coordinated pump-and-dump schemes targeting tiny Nasdaq stocks, including a series of initial public offerings lead-underwritten by Bancroft Capital LLC. Bancroft is based in Fort Washington, Pennsylvania, a certified Service Disabled Veteran Owned investment business founded and led by Cauldon D. Quinn. The Inquirer framed the question the lawsuit raises in language worth quoting directly. Was Bancroft Capital a "hapless victim or greedy enabler."

That is the entire question. The answer will come out of discovery or it will not come out at all. But the pattern around the question is already in the public record, and the pattern is what readers like Marcus need.

The pattern has a name. The SEC and the FBI call it ramp and dump. It is the social media descendant of the old boiler room. I worked one of those rooms in Chicago when I was younger than my own son is now. A hundred desks, a hundred phones, a hundred guys reading the same script off the same paper taped to the same particleboard. The pitch was metals. The mark was a dentist in Ohio. The close was urgency. We did not need a Series 7 because we were not selling securities. We were selling palladium that mostly existed on a piece of paper.

The new room does not have desks. The new room is a WhatsApp group with four hundred members and a pinned message and an admin who calls himself an analyst. The mark is Marcus in his truck in a warehouse parking lot. The close is the same close. Urgency. Scarcity. Social proof. Authority. The pen at hour five.

Here is how the machine is built, based on warnings published by the SEC, FBI, and FINRA, and based on the pattern documented in multiple recent federal complaints.

A small company, often a foreign issuer, often valued at fifteen million dollars or less, files to go public on Nasdaq. The IPO is priced low, typically between four and six dollars. The float is tiny. Pre-IPO shares are distributed to insiders and affiliated parties at little or no cost. The shares can be sold the moment the stock starts trading.

The social media operators then manufacture demand. WhatsApp groups. Telegram channels. Facebook ads. Instagram reels. Discord servers. Increasingly, deepfake videos of recognizable financial figures who never agreed to appear in them. The operators tell their members the stock is about to run. They tell them the entry window is closing. They tell them to buy at the open on IPO day.

The buyers buy. The price goes up because the float is tiny and the buying is concentrated. The chart looks like the chart the analyst promised. New members of the group see the green and the screenshots and they buy too. The insiders sell into the demand. The price collapses. The group goes silent. The channel disappears.

The FBI reported a 330 percent increase in pump-and-dump complaints over the last year. At an April 15, 2026 House Financial Services Committee hearing, Subcommittee Chairman Ann Wagner noted that investment scams accounted for nearly half of the twelve billion dollars Americans lost to financial exploitation in 2024, a 24 percent increase from the previous year. She used the specific phrase "ramp-and-dump schemes where scammers ramp up a stock's price through bots and fake accounts."

The pattern shows up in case after case.

Ostin Technology Group. A securities class action filed in February 2026 alleges a scheme that pushed the stock up over 1,100 percent in two months before it collapsed in a single day, wiping out roughly $950 million in market value.

Concorde International Group, ticker YOOV. A class action filed in March 2026 alleges the stock surged from an IPO price of four dollars to $31.06 before crashing roughly 80 percent to $5.66 in a single day on July 10, 2025.

China Liberal Education Holdings. In March 2025, federal prosecutors seized $214 million in proceeds from a scheme involving the Cayman Islands-based company. Victims lost nearly everything.

Every one of those stocks had an underwriter. Underwriters are the firms that walk a company through the IPO door. They certify, in effect, that the offering is real enough to list. They sign the paperwork. They take a fee.

The lawsuit reported by the Inquirer asks whether one Fort Washington underwriter, Bancroft Capital LLC, lead-underwrote a series of these tiny IPOs in 2024 and 2025 without knowing what would happen to them after the bell rang, or whether the firm was part of the door. Bancroft has not been found liable. The question is alleged, not proven. Allegation is not adjudication. Those cases remain ongoing.

But read this slowly. Five poorly performing tiny IPOs from the same lead underwriter inside an eighteen-month window is not turbulence. It is a pattern. Patterns are not proof. Patterns are why the lawsuit exists.

Nasdaq has started to respond. In December 2025, with SEC approval, the exchange tightened its listing rules. A $25 million minimum offering proceeds requirement for companies principally operating in China. A $15 million minimum public float for new listings. The SEC stood up a Cross-Border Task Force to Combat Fraud in September 2025. The U.K.'s FCA led a coordinated week of action with seventeen global regulators on May 7, 2026, targeting illegal finfluencing. The takedown requests went out across platforms.

The takedown requests will not reach Marcus. The takedown requests reach the next group. The current group is already gone. The admin has a new handle. The new group has a different name and the same pinned message.

Marcus sat at the kitchen counter the night the position went red and stared at his phone. He did not tell his wife for two days. When he did tell her, he did it in the truck, on the way to her mother's house, because he could not look at her face and say the number out loud at the kitchen table. The number was just over seven thousand dollars. The truck fund was now the lesson fund. He did not call it that. I am calling it that.

He did one thing right. He kept the screenshots. He kept the WhatsApp messages he had managed to save before the group was deleted. He filed a complaint with the SEC. He filed a complaint with the FBI's IC3 portal. He did not get his money back. He may never get his money back. But he is in the record now, which is the only place the next investigation can find him.

Picture the room one more time.

A four-hundred-member WhatsApp group with a pinned message that says "education only." An admin in a navy suit. A small Nasdaq IPO opening at six dollars. A buy order placed from a warehouse parking lot at 9:28 in the morning. A green candle that lasts two hours. A red candle that lasts two days. A truck that does not get replaced. A wife who does not get the surprise.

And somewhere above all of that, a filing on EDGAR with an underwriter's signature on it.

The lawsuit asks whether the signature was a hand on the door or a hand on the trigger. The discovery will answer that or it will not. The machine does not need the answer. The machine needs the next group, the next IPO, the next Marcus in the next parking lot.

He was not the investor.

He was the bid.

- The Philadelphia Inquirer | May 12, 2026 | "Social media 'pump and dump' fraudsters targeted tiny Nasdaq stocks, including this Philly firm's IPOs, says lawsuit"

- House Financial Services Committee | April 15, 2026 | Subcommittee hearing on securities fraud, remarks of Chairman Ann Wagner

- FBI | 2025-2026 | Reported 330% increase in pump-and-dump complaints

- Nasdaq / SEC | December 2025 | Approved listing rule changes including $25M minimum offering proceeds requirement for China-principal issuers and $15M minimum public float

- SEC | September 2025 | Cross-Border Task Force to Combat Fraud established

- UK FCA | May 7, 2026 | Coordinated international week of action targeting illegal finfluencing, 17 regulators participating

- Securities class action filing | February 2026 | Ostin Technology Group, alleged scheme pushing stock 1,100%+ before single-day collapse

- Securities class action filing | March 2026 | Concorde International Group (NASDAQ: YOOV), lead plaintiff deadline May 20, 2026

- DOJ | March 2025 | $214M seizure related to China Liberal Education Holdings Ltd. pump-and-dump

- Class action against Meta Platforms Inc. | March 25, 2026 | Allegations regarding scam ad enablement of $500M pump-and-dump scheme

- Bancroft Capital LLC | Public record | Fort Washington, PA-based SDVOSB investment firm, founder/CEO Cauldon D. Quinn, lead underwriter on series of 2024-2025 Nasdaq IPOs

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.