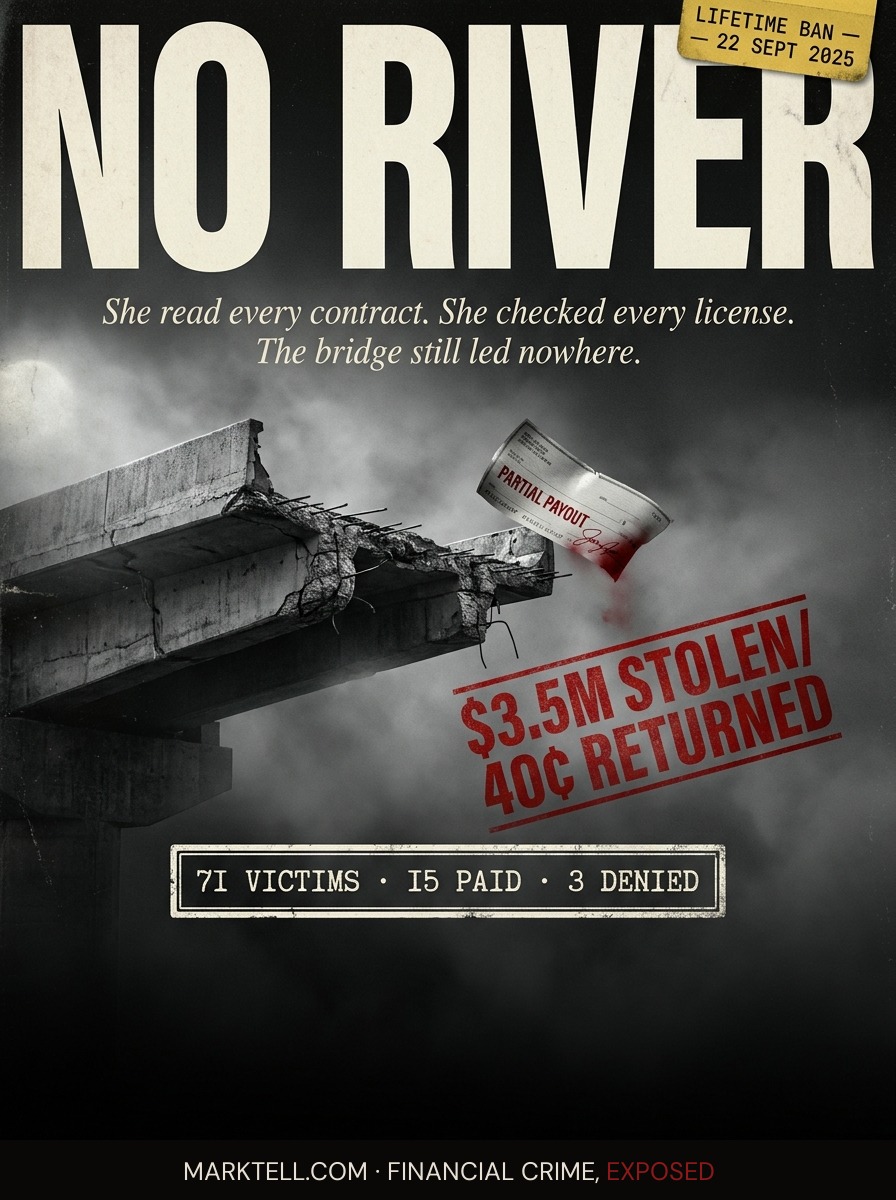

The bridge loan that crossed no river, and the fund that paid out forty cents

A Calgary realtor sold bridge loans for real estate deals that never existed. Four years later, Alberta's regulator cut the largest assurance fund cheque in its forty-year history. It covered less than half the loss.

Margaret read contracts for a living.

Thirty-one years of bookkeeping for two dental practices and a print shop in Calgary's southeast. She knew what a signature block was supposed to look like. She knew the difference between a promissory note and a loan agreement. When her husband died in 2021 and the life insurance came through, she put most of it into GICs because that is what careful people did. She kept a smaller piece liquid because a friend from the bookkeeping circuit had mentioned that her son-in-law, a realtor at Re/Max Central, was sometimes looking for short-term private money for bridge loans. Six months. Twelve percent. Secured against a property that was about to close.

Margaret had read bridge loan agreements before. They were not exotic. A buyer needed cash to close on a new house before the old one sold. A lender filled the gap. It was the kind of arrangement that lived in the boring middle of real estate, the part nobody wrote books about.

She met Eric Drinkwater for coffee in late 2022. He had a business card with the Re/Max Central crest. He had a brokerage. He had a managing broker whose name was on the wall. He had what looked like a closing schedule on his iPad, with addresses and dates and lawyer's names.

She wrote him a cheque for $80,000.

For fourteen months, the interest arrived on time.

That part may be the part Margaret thinks about most.

II. The bridge

There is a thing a Ponzi scheme does that is not really about the lie. The lie is the easy part. The harder part is the architecture that makes the lie sit still long enough to be believed. In Drinkwater's case, the architecture had a name people in real estate use without thinking. The bridge loan.

A bridge loan, in plain English, is short-term money that covers a gap. The borrower needs cash now and will have cash later. A lender, often a private one, fills the gap and earns a high interest rate for the inconvenience. Real estate runs on these arrangements. They are not unusual. They are not suspicious.

That is what made them perfect.

According to the Real Estate Council of Alberta, the provincial regulator that licenses realtors and administers a consumer protection fund, Drinkwater was soliciting bridge loans for transactions that did not exist. The properties were not closing. There were, in many cases, no properties. There were no buyers. The closing schedule on the iPad was a stage set.

RECA's adjudicated findings say Drinkwater admitted to soliciting fraudulent bridge loans. He received a lifetime ban from trading in real estate in Alberta, effective September 22, 2025, and was ordered to pay $9,500 in hearing costs. The Calgary Police Service charged him with one count of fraud over $5,000 in May 2025. That case is ongoing.

The scheme is believed to have operated between March 2020 and February 2024. RECA says at least 71 people lost more than $3.5 million.

The interest cheques that arrived on time for fourteen months were paid with money from people who came in after Margaret.

III. The fund

Alberta is one of the few provinces with a consumer protection fund for victims of real estate licensee fraud. It is called the Real Estate Assurance Fund. Licensed real estate professionals pay into it. When one of them does what Drinkwater did, the fund is supposed to make the victims partially whole.

On May 10, 2026, RECA approved $1,407,875.70 in compensation for fifteen Drinkwater victims. It is the largest single payout in the fund's forty-year history.

Read the math slowly.

$3.5 million lost. $1.4 million returned. Seventy-one victims. Fifteen claims paid. Three claims denied for eligibility.

The fund pays a maximum of $35,000 per transaction. That number is set by provincial legislation. It does not move because the loss was larger. Margaret lent Drinkwater $80,000. If she filed and qualified, the most she could get back was $35,000. If she had been promised twelve percent interest and lost two years of payments, none of that counted. Projected profits are not covered. Lending fees are not covered. Inducements are not covered.

The fund covers the principal you wrote on the cheque, up to a cap, and only if you can prove a licensee committed fraud or breach of trust against you in a way the regulator recognizes.

Derek Davidson, a named victim who lent Drinkwater $80,000, received $73,000 across multiple transactions. He told reporters the payout took too long and raised questions about whether the regulator had been doing its job.

He is correct on both counts.

IV. The uncle

This is where the bridge starts to look less like a single realtor's lie and more like a structure with rooms above it.

RECA has issued hearing notices against two other licensees connected to Re/Max Central. Pat Hare, the brokerage's former owner, is Drinkwater's uncle through marriage. David Lem was the managing broker. The regulator alleges Hare became aware of the scheme around 2021 and received payments from Drinkwater. Lem was the licensee responsible for supervising trades at the brokerage.

These are allegations. Neither has been adjudicated. Both are entitled to a hearing and a defense.

But place the dates next to each other.

The scheme is believed to have started in March 2020. RECA alleges Hare became aware around 2021. The scheme continued until February 2024. Re/Max Canada terminated the Re/Max Central franchise agreement in May 2025. RECA's then-board chair was replaced in November 2025 after public scrutiny of how the regulator had handled the case. The payout came in May 2026.

Six years from the first cheque to the first cheque back.

V. The chair

Margaret got her letter from RECA in early 2026. The cheque was for $35,000. She had written one cheque, for $80,000, so under the legislation that was the maximum she qualified for.

She read the letter at the kitchen table where she had read the bridge loan agreement four years earlier. The reading glasses were the same. The table was the same. The signature block at the bottom of the RECA letter was a regulator's signature, which is the kind of signature that arrives when something has already gone wrong.

She thinks about what she saw, and what she did not see, and whether the difference between the two was knowledge or vocabulary.

She had read the agreement. She had checked the brokerage. She had seen the iPad with the closings on it. She had received interest payments on time for over a year. The thing she could not see was the thing the structure was designed to hide. The properties did not exist. The closings did not exist. The interest was other people's principal.

The bridge crossed no river.

That is the part of these cases that does not get easier to write. The mark is not careless. The mark is doing exactly what careful people are told to do. Read the paperwork. Check the license. Ask for collateral. Verify the brokerage. The machine is built to survive all of that. It is built specifically to survive the kind of person who does her homework.

Margaret is a composite, but the kitchen table is not. The cap is not. The forty cents on the dollar is not. The six years is not.

The fund did what it was designed to do. The legislation did what it was written to do. The regulator paid out the largest single amount in its history. And the victims got back less than half.

Read that again.

The system worked. And the loss was still permanent.

That is the part the bridge loan was built to leave behind.

- Calgary Herald | May 15, 2026 | "Alberta regulator pays out $1.4M to victims of real estate Ponzi scheme"

- Real Estate Council of Alberta | May 10, 2026 | RECA announcement of Real Estate Assurance Fund payout for Drinkwater victims

- Real Estate Council of Alberta | September 22, 2025 | Drinkwater lifetime ban order and hearing costs

- Calgary Police Service | May 2025 | Fraud over $5,000 charge against Eric Drinkwater

- Real Estate Council of Alberta | 2025-2026 | Hearing notices against Pat Hare and David Lem

- Re/Max Canada | May 2025 | Termination of Re/Max Central franchise agreement

- Real Estate Council of Alberta | November 2025 | Appointment of Cynthia Moore as board chair

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.