The auditors and the lawyers wrote sixty-six million dollars worth of "we did nothing wrong."

FTX's former law firm Fenwick & West and its auditor Prager Metis agreed to pay roughly $66 million to settle customer fraud claims, while Fenwick still faces a separate $525 million suit and denies knowing anything was wrong.

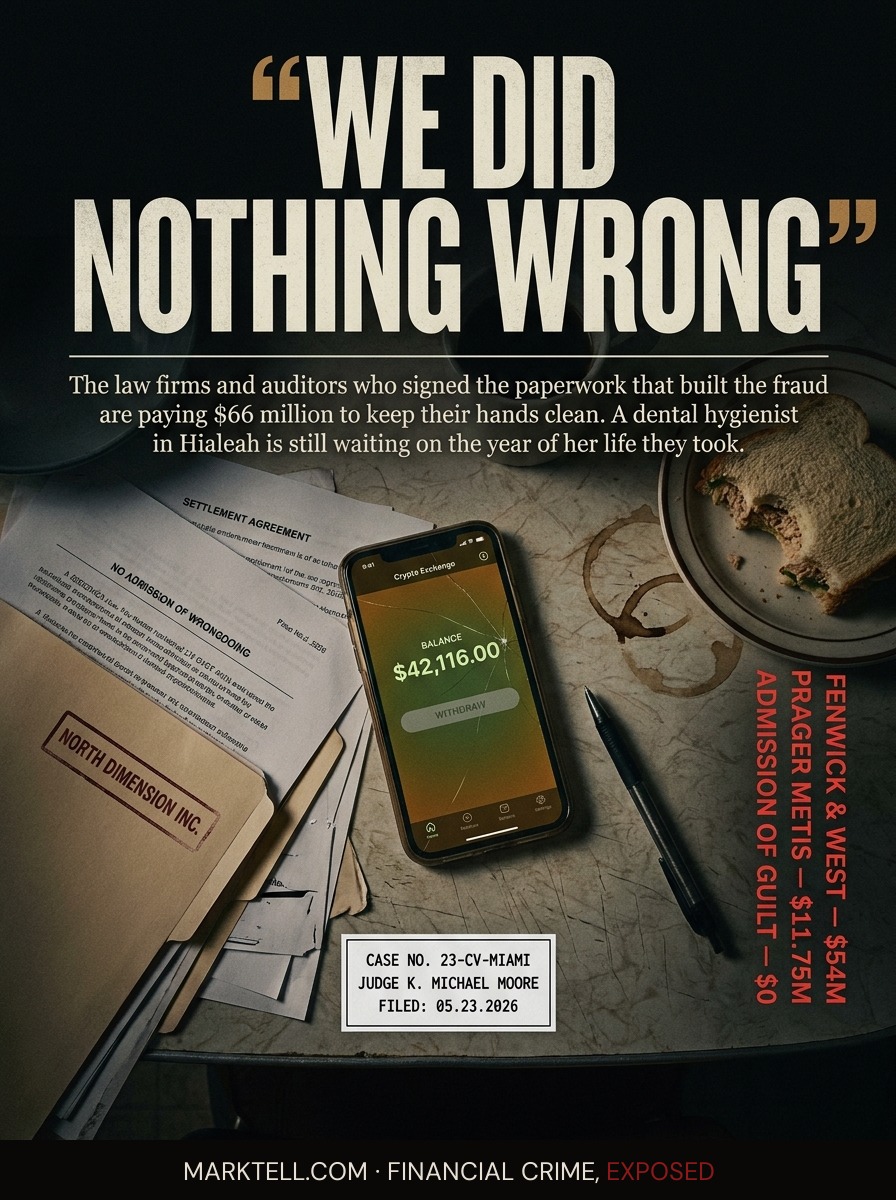

Marisol sat at her kitchen table in Hialeah on the afternoon of November 8, 2022, with her phone in one hand and a tuna sandwich in the other. She was fifty-eight years old. She cleaned teeth for a living, four days a week, and she had been doing it for thirty-one years. The kitchen table was where the mail piled up and where she did her bills on Sunday nights. The phone was open to the FTX app.

She tapped the withdrawal button. Nothing happened.

She tapped it again. Then she put the sandwich down and tapped it with both thumbs, the way you do when a thing is not working and you are starting to understand that it is not going to.

Her balance still showed $42,116. The number was right there. The number had been right there for ten months. Her nephew Hector had shown her the FTX commercial during the Super Bowl in February. Tom Brady was in it. Larry David was in it. Steph Curry was in it. Hector said the exchange was audited. Hector said it was the safest one. Hector was twenty-six and worked in IT and Marisol trusted him the way you trust the youngest person in the family who knows about computers.

She had wired the money over three deposits. The biggest one was $25,000, which was most of what she had saved after her mother's funeral. The smallest was $5,000, which she sent the day her car needed brakes and she decided she could pay for the brakes with overtime and let the $5,000 grow instead.

The withdrawal button did not work that afternoon. It did not work that evening. It did not work the next morning. On November 11, FTX filed for bankruptcy in Delaware and Marisol learned, slowly, over a week of news stories she did not entirely understand, that the safest exchange was not safe and the audited financials were not what audited meant and the money she thought was sitting in a digital account had been moved, while she slept, into a hedge fund called Alameda Research that had been losing it.

Hector did not call her. She called him. He cried a little, on the phone. She did not.

That part may be the saddest.

I.

On Friday, May 23, 2026, three and a half years after Marisol tapped that button, two of the firms that signed the paperwork on FTX's legitimacy agreed to pay $66 million to settle customer claims.

Fenwick & West, the Silicon Valley law firm that served as FTX US's principal outside counsel, agreed to pay $54 million. Prager Metis, one of the accounting firms that audited FTX's books, agreed to pay $11.75 million. A former Miami Heat forward named Udonis Haslem, who had taken money to promote the exchange, agreed to pay $420,000.

The settlements were filed in federal court in Miami in front of U.S. District Judge K. Michael Moore. They are preliminary. They require approval. The lawyers running the customer side are David Boies and Adam Moskowitz, the same names that have been working the FTX recovery for years.

Fenwick & West denied wrongdoing. The firm's statement said it was "not aware of the fraud at FTX." It said it stood by its legal work.

Read that slowly. The law firm that allegedly helped set up the corporate structures the fraud ran through is paying $54 million to make customer claims go away while telling the public it did nothing wrong.

This is what a settlement looks like when you do not want to admit anything and you also do not want to find out what twelve people in a jury box will think after six weeks of testimony.

II.

The thing that makes FTX a true-crime story instead of just a bankruptcy is the room around the room.

Sam Bankman-Fried is in federal prison serving 25 years. He was sentenced in 2024 after a jury found he had stolen billions from customers. That part is closed. The founder has been processed.

The professional services machine around him has not been.

A crypto exchange is not a building. It is a stack of paperwork. The paperwork is what tells regulators, banks, customers, and reporters that the thing is real. The paperwork is drafted by lawyers. The financial statements are signed off on by auditors. The commercials are read by athletes and comedians who are paid a fee. The exchange is the front. The paperwork is the foundation.

Plaintiffs allege Fenwick & West did not just review FTX's paperwork. They allege the firm helped build it. Specifically, the complaint alleges Fenwick advised on the creation of North Dimension Inc., a shell entity that plaintiffs say was used to route over $3 billion in customer funds away from where customers thought their money was sitting and into the bank accounts Alameda Research used for trading.

A shell entity is a company that exists on paper. It has a name. It has an address. It has a bank account. It does not have employees or a business in the way you would recognize a business. Its job is to be a name on a wire transfer so the money looks like it is going somewhere ordinary.

Nishad Singh, FTX's former director of engineering, pleaded guilty and testified at SBF's trial. According to his testimony, he informed Fenwick attorneys about the misuse of customer funds. The firm disputes the characterization.

These are allegations. They have not been adjudicated. The settlement is being paid without an admission. Allegation is not the same as proof.

But here is what is in the record. The SEC charged Prager Metis with negligence-based fraud in September 2024. The agency said the accounting firm lacked the competence to audit a crypto exchange, failed to understand the relationship between FTX and Alameda, and issued audit reports that falsely claimed compliance with Generally Accepted Auditing Standards. Prager Metis paid $1.95 million to settle the SEC charges without admitting or denying the findings.

The audit said the books were good. The books were not good. The auditor was charged with not being qualified to know the difference.

III.

Picture Marisol's kitchen table in February of 2022. The Super Bowl is on. The commercial plays. Tom Brady. Larry David. Steph Curry. The exchange is "FTX." The pitch is that crypto is finally grown up.

Now picture, in some office somewhere in Silicon Valley or New York or Miami, the paperwork being drafted that would let the deposits route through a company called North Dimension. Picture the audit being signed.

The press release got the Super Bowl ad. The filing got the shell company.

The thumbnail got Tom Brady. The footnote got the auditor's signature.

The customer got the app on her phone. The customer's money got the wire instructions to North Dimension.

This is the architecture of how a fraud of this size happens. It does not happen because one person is a criminal. It happens because a network of professionals signs the documents that make the criminal look like a CEO.

When the network signs, the network gets paid. When the fraud collapses, the network says it did not know.

IV.

The customer side of FTX has done better than most fraud victims ever do. The bankruptcy estate, under restructuring expert John J. Ray III, has distributed more than $5 billion to creditors. A $2.2 billion distribution went out on March 31, 2026. Some creditor classes are seeing recovery rates of 100% or more, measured against their dollar value at the time of the November 2022 collapse.

Measured against what those balances would be worth today if the exchange had not collapsed and crypto prices had kept moving, the recovery is something else.

Marisol got most of her money back. Not all of it. The $42,116 came back as roughly that, paid out in tranches over 2024 and 2025, dollar for dollar at November 2022 valuations.

What she did not get back is the year she spent thinking she was stupid. The conversations with her sister where she said she should have known. The Sunday nights at the kitchen table where she went through the FTX statements she had printed out and tried to figure out what she had missed.

She had not missed anything. The paperwork was designed to be missed.

V.

The $66 million settlement in Miami is not the end of the professional services chapter of the FTX story.

A separate lawsuit is pending in Washington D.C., filed around May 14-16, 2026, by a group of twenty FTX victims. That suit seeks $525 million from Fenwick & West as an institution and from several individual partners. It is not covered by the Miami settlement. Fenwick will be defending it.

So the firm that says it did nothing wrong is paying $54 million in Miami to make one set of claims go away while preparing to spend the next several years explaining, in Washington, why it should not pay another $525 million for the same conduct.

The math on that posture is its own kind of confession.

VI.

The reframe is simple. Sam Bankman-Fried was the face. The lawyers and the auditors and the celebrities were the frame around the face. Without the frame, no one would have looked at the face.

When a fraud collapses, the country prosecutes the face. The frame keeps its license, pays a settlement, and waits for the next exchange to call.

That is the machine. It does not get arrested. It gets retained.

Marisol still has the manila folder on her kitchen table. The statements are still in it. She keeps them because she wants to remember what audited looked like before she knew what audited did not mean.

- The Block | May 23, 2026 | https://www.theblock.co/post/402425/ftxs-former-law-firm-auditor-agree-to-pay-66-million-to-settle-customer-claims-over-fraud

- SEC press release | September 2024 | SEC charges against Prager Metis for FTX audit failures, $1.95M settlement

- U.S. v. Bankman-Fried | 2024 | Sentencing to 25 years, S.D.N.Y.

- FTX Recovery Trust | March 18, 2026 | Announcement of $2.2B distribution to creditors, disbursed March 31, 2026

- Nishad Singh trial testimony | 2023 | U.S. v. Bankman-Fried

- FTX Chapter 11 filing | November 11, 2022 | District of Delaware

- Washington D.C. lawsuit against Fenwick & West | filed approximately May 14-16, 2026 | seeking $525M from 20 FTX victims

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.