The auditor said wait. The CFO published anyway.

In the summer of 2020, a Minnesota electronics plant invented work that was never done to make a quarter look like growth. Five years later, the SEC named the men who let the number go out.

Diane was sixty-two and three years into retirement when she opened the brokerage app on the morning of January 26, 2021. Her coffee was still too hot. The kitchen in Spokane was quiet. Her husband was still upstairs. She owned four hundred shares of Key Tronic because her brother-in-law had worked at the Oakdale plant in Minnesota for nineteen years and had told her, the way family tells you these things at Christmas, that it was a steady company. Not exciting. Steady.

The app showed green. Quarterly earnings had beaten the prior year. Net income of $1.58 million. EPS up six cents year over year. She did not read the press release. She read the color. Green meant the brother-in-law was still right.

Five years later, the Securities and Exchange Commission would explain, in the patient prose of an administrative order, what was inside that green.

I.

The plant in Oakdale is a contract manufacturing facility. Key Tronic builds electronics for other companies under their names. Medical devices. Industrial controls. The kind of work that does not show up in a Super Bowl commercial. In the summer of 2020, the orders started slowing. Then they stopped slowing and started falling. The forecast shortfall at Oakdale was first $5 million. Then $10 million. People on the floor began to think about layoffs the way people in manufacturing towns think about layoffs, which is to say: by counting cars in the parking lot.

Key Tronic uses something called absorption accounting. The plain English version is this: when a plant is making things, the cost of running the plant gets spread across the things it is making. Empty plants are expensive on paper, because the rent and the salaries and the lights are still there, but there is nothing to absorb them. A plant with no work generates loss the way a plant with work generates profit. Both come out of the same arithmetic.

So somebody at Oakdale solved the arithmetic. According to the SEC's administrative order, employees entered figures into the inventory system showing raw materials as work-in-process. Work-in-process means: we are building it. We have started. The cost is being absorbed. The internal name for these entries, the order says, was the "Monster Job."

There was no monster job. There was no work happening on those materials. The entries were reversed at the start of the next month and put back in again. Reversed. Put back in. Each cycle pulled income into the period that needed it.

The order says this practice improperly increased income by close to $1 million across the first half of fiscal 2021.

II.

On the morning of the January 2021 earnings release, an internal complaint reached the company. Someone, inside, said something was wrong.

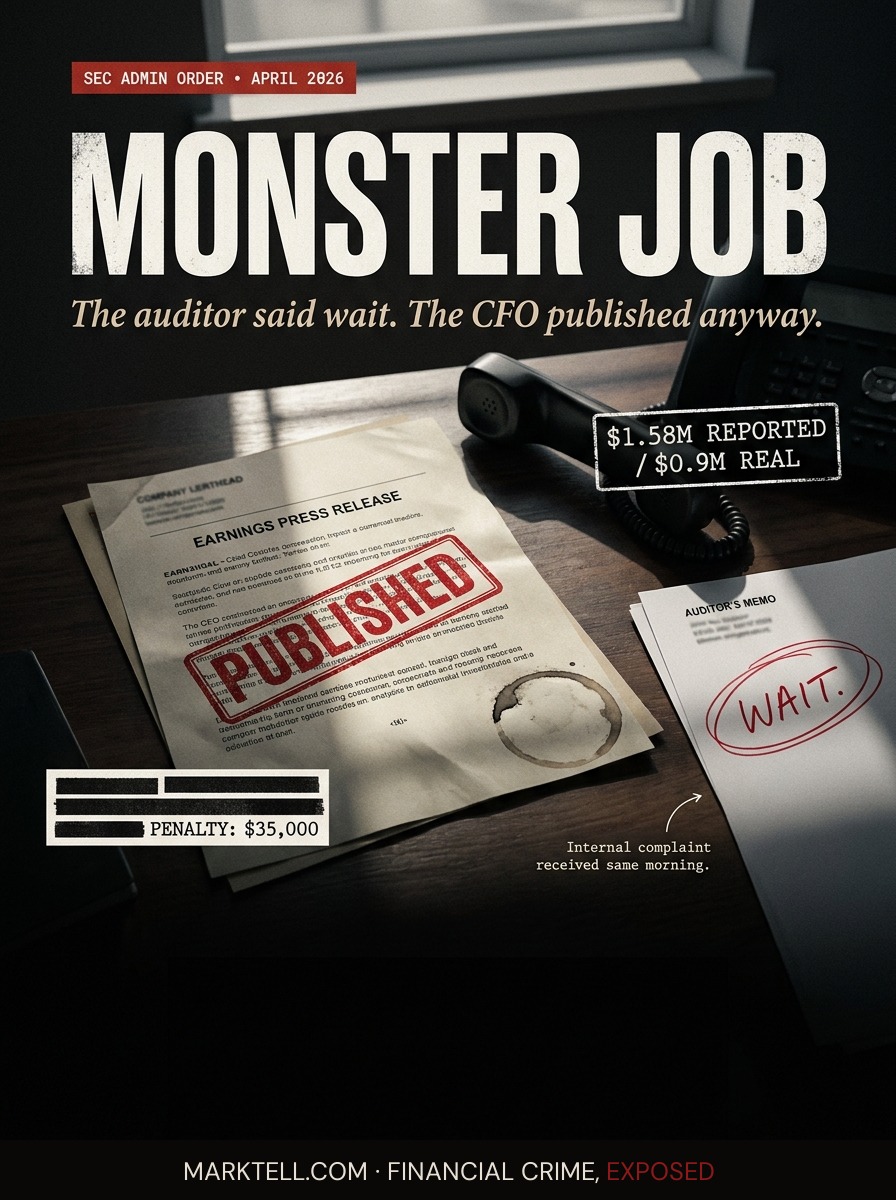

The auditor said something too. According to the SEC order, the auditor advised Key Tronic to consider postponing the release. The auditor offered specific language to soften the numbers, noting that the data was "preliminary and could be subject to change."

Brett Larsen was the Chief Financial Officer. He is the Chief Executive Officer now.

The release went out.

The order says Larsen's materiality analysis was insufficient. Read that slowly. The CFO of a public company received a warning from the company's own auditor and an internal complaint on the same morning, ran a calculation about whether the questionable amounts mattered, and decided they did not matter enough to wait. The number on Diane's screen was the result of that decision.

Nicholas Fasciana, the Senior Vice President of U.S. Operations, oversaw the Oakdale plant. The SEC found he was aware of and directed some of the misconduct.

III.

Picture the math the way the SEC laid it out.

Reported Q2 FY2021 net income: $1.58 million. Corrected for the out-of-period adjustments: roughly $0.9 million. A drop of about forty-four percent.

Reported year-over-year EPS growth: six cents. Corrected: zero.

Not a beat. A flat quarter. Possibly worse. The whole shape of the story Diane saw in green on her phone, the shape her brother-in-law confirmed at Christmas, depended on the difference between $1.58 million and $0.9 million. The difference was the Monster Job.

On February 11, 2021, Key Tronic publicly disclosed the inventory irregularities. The stock fell. Diane saw the red this time. She did not sell. She did what a lot of long-term holders do. She told herself it was a one-time thing. She told her husband it was a one-time thing. She kept the shares.

IV.

The SEC announced the settled charges on April 20, 2026.

Key Tronic agreed to a cease-and-desist order for violating Sections 13(b)(2)(A) and 13(b)(2)(B) of the Securities Exchange Act of 1934. Those are the books-and-records and internal-controls provisions. In plain English: a public company has to keep accurate records and has to have systems that catch the inaccurate ones. The SEC found Key Tronic's systems did not.

The company paid no civil penalty. The order credits cooperation and remedial efforts.

Brett Larsen, the then-CFO and now CEO, agreed to a cease-and-desist for causing the company's violations. He paid $20,000.

Nicholas Fasciana, the SVP of U.S. Operations, agreed to a cease-and-desist for violating Section 13(b)(5) and Rule 13b2-1 and for causing the company's violations. He paid $15,000.

No one was charged with fraud. No one admitted or denied the findings. That is how SEC settlements end. The order is the record. The fines are the receipt.

$35,000 total in individual penalties for a misstatement that, by the SEC's own arithmetic, would have erased the quarter's growth.

V.

The defense bar has already started using this case. Articles published in mid-May 2026 cited the Key Tronic order as a "helpful reference point" for other public companies in settlement discussions. That is lawyer language. It means: if your client cooperates and remediates, you can argue for this outcome. No fraud charge against the company. No corporate fine. Two small individual penalties. A cease-and-desist that prohibits doing the thing you already stopped doing.

This is not an indictment of the SEC. The agency has limited resources and made a judgment about what cooperation buys. It is a description of the price.

The price for inflating a quarter by close to a million dollars and letting the release go out over the auditor's caution was thirty-five thousand dollars in individual penalties, an administrative order, and five years of distance.

VI.

Diane still owns the shares. The plant in Oakdale is part of a larger story now. Key Tronic is moving manufacturing to Juarez and Vietnam and winding down in China. The Q3 FY2026 release earlier this month showed revenue down to $89.6 million from $112 million the year before but margins improving. The stock went up on the news. The market is looking forward.

Diane is sixty-seven now. She does not check the app the way she used to. Her brother-in-law retired in 2023. He is still proud of his nineteen years. He should be. The work he did at Oakdale was real.

The Monster Job was the other thing. The work that was not done. The entries that made the empty plant look full. The number on the screen that was not the number.

That is what Diane lost. Not money. The thing money is supposed to be made of.

The auditor said wait. The CFO published anyway. Five years later, the SEC wrote it down.

- SEC Administrative Order, In the Matter of Key Tronic Corporation, Brett Larsen, and Nicholas Fasciana | April 20, 2026 | SEC press release and order

- Grit Daily | May 28, 2026 | "Key Tronic Executives Settle SEC Charges Over Fake 'Monster Job' Inventory Scheme at Minnesota Facility"

- Key Tronic Corporation | February 11, 2021 | Public disclosure of inventory irregularities

- Key Tronic Corporation Q3 FY2026 Earnings Release | May 5, 2026

- Securities Exchange Act of 1934, Sections 13(b)(2)(A), 13(b)(2)(B), 13(b)(5), Rule 13b2-1

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.