He told the court he was good with money. The ledger told the rest.

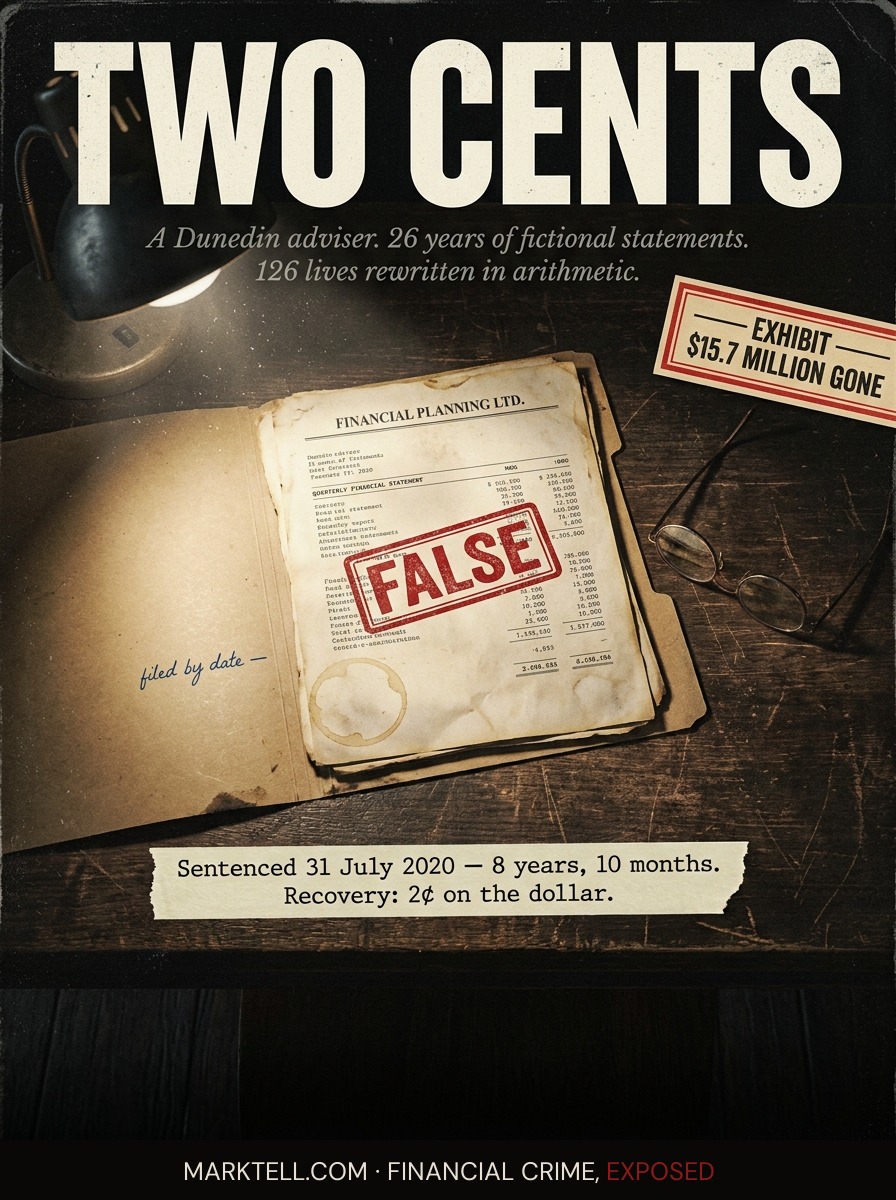

For more than two decades, Barry Kloogh sat across from Dunedin retirees and told them their money was working. It wasn't. The Serious Fraud Office put the loss at $15.7 million. The liquidator now says recovery will be roughly two cents per dollar invested.

Margaret kept the statements in a manila folder in the sideboard. She was 71, retired from a primary school in Mosgiel, and she had been a client of the same Dunedin financial adviser for more than a decade. The statements arrived on quarter ends. She filed them by date. Her husband had done the same with the power bills until he died, and she had taken over the system without changing it.

The number on the page in late 2018 was the number she expected. A little more than last quarter. A modest, believable amount of growth. The letterhead said Financial Planning Ltd. The signature was the one she knew.

She did not know yet that the number was a fiction. She did not know that the paper in her hands was, in the language of the eventual charge sheet, a false statement by a promoter. She knew only that the adviser had told her things were working, and the paper in the folder said they were working.

That folder is the story. Not the man. The folder.

I.

His name is Barry Edward Kloogh. He worked in Dunedin. He was the sole director and shareholder of Financial Planning Ltd and Impact Enterprise Limited, two companies he used as the front of the desk. Behind the desk was the machinery: client money moving into accounts he controlled, statements generated to look like investment performance, new money paying out the people who asked for withdrawals.

That is a Ponzi scheme. The polite definition is that returns to existing investors are paid from the capital of new investors rather than from genuine profit. The honest definition is that there is no investment. There is a name on a letterhead and an arithmetic problem that only works as long as more money comes in than goes out.

Kloogh ran his version of that arithmetic problem from 1993 to mid-2019. Twenty-six years. The Serious Fraud Office, New Zealand's lead agency for serious financial crime, put the loss at $15.7 million. The liquidator's later reports moved the figure above $16 million. At least 126 claimants were identified. Most of them were people like Margaret.

II.

The pitch was not elaborate. It did not have to be.

Kloogh hosted dinners. Free ones. Potential clients were invited to hear about retirement planning over a meal. The Serious Fraud Office later described the technique plainly: he enticed clients with hospitality and then directed their money into his own operations.

Picture the room. A function space at a Dunedin hotel. Tablecloths. A printed agenda. A man in a suit who knows the names of your grandchildren by the second meeting. He uses words like diversification and managed and your money is being looked after. He does not ask you to take a risk. He asks you to stop worrying.

Margaret went to one of those dinners around 2007. She does not remember the menu. She remembers that the adviser shook her hand at the door and asked about the school she had taught at.

III.

The mechanism, once she signed on, was almost mundane.

She would write a cheque, or arrange a transfer, into an account associated with one of his companies. He would tell her where it had been invested. A quarterly statement would arrive showing that investment and its supposed performance.

The statement was the machine.

According to the SFO, Kloogh provided clients with false or forged documents, including false investment statements. He was charged with false accounting and forgery alongside the deception and theft counts. He pleaded guilty to all of it in March 2020.

The 11 representative charges, in the language of the case, were false accounting, false statements by promoter, theft by a person in a special relationship, obtaining by deception, and forgery. Read that list slowly. Each charge is a different kind of paper. Each one describes a different way that a piece of paper can lie.

The paper is what kept Margaret in the chair for twelve years.

IV.

Where the money actually went is not a mystery. The SFO and the liquidator have laid it out.

It went to his business, meaning the rent and salaries and the costs of running the office where the statements were printed. It went to travel. It went to cars. It went to loans to family. And it went to pay the clients who asked to withdraw, because that is the only way a Ponzi keeps running. The withdrawal of one client is funded by the deposit of another. Eventually the deposits do not arrive fast enough, and the machine seizes.

In mid-2019, the machine seized. The Financial Markets Authority, New Zealand's securities regulator, became aware of the fraud and referred the matter to the SFO. Kloogh's financial adviser authorisation was cancelled in September 2019. By March 2020, he had pleaded guilty.

On 31 July 2020, he was sentenced to eight years and ten months in prison, with a minimum non-parole period of five years and four months.

V.

Now do the math the way Margaret had to.

She had invested across years. She does not want her exact number printed. Say it was a six-figure sum, retirement money, the proceeds of a house she sold when her husband died.

The liquidator's most recent report, dated 13 March 2026, estimates that clients are likely to recover roughly 2 cents for every dollar invested. An earlier estimate had been 2.5 cents. The number has moved in the wrong direction.

So a client who handed over $200,000 over the years is, on current estimates, looking at $4,000.

Not down. Gone.

The official assignee, who is the public officer in New Zealand responsible for administering bankrupt estates, was as of March 2026 expecting to recover $455,442 from the sale of property associated with two trusts linked to Kloogh. Investors are owed around $15 million. Do that division. The denominator swallows the numerator.

A May 2023 High Court judgment ordered $426,107 from one property sale to the official assignee. $40,823 went to Kloogh's wife, Svetlana Spectra, who argued her own contributions and her lack of knowledge of the fraud. The court accepted part of that argument. The clients did not get the $40,823.

VI.

There is a sentence Kloogh said, in the course of the proceedings, that became the headline. He said he was good with money management.

Read that slowly.

He said it about himself, in connection with a case in which he had pleaded guilty to false accounting, false statements, theft, obtaining by deception, and forgery. He said it about a 26-year operation in which the recovery rate for his clients will be roughly 2 cents on the dollar.

What he meant, almost certainly, is that he was good at the management of the appearance of money. Good at the statements. Good at the explanations at the dinners. Good at sitting across the desk from a retired teacher and telling her things were working when the only thing working was the printer.

That is a real skill. It is not the skill he was licensed for.

VII.

The FMA released a "lessons learned" report on this case in October 2023. The polite framing was that the scheme's longevity was partly due to its sophistication and the regulatory regime at the time. The Financial Advisers Act 2008, under which Kloogh operated for most of the relevant period, has since been repealed and replaced. The new regime requires Financial Service Provider registration and annual returns. The FMA is developing guidance for custodians to ensure clients receive mandated custody reports.

A custody report, in plain English, is a statement from the entity that actually holds your money, sent independently of your adviser. If Margaret had received one of those, the gap between Kloogh's statement and reality would have been visible on a single piece of paper.

She did not receive one. The regime did not require it. The machine ran in the gap.

VIII.

Margaret found out the way most of the clients found out. Not from a phone call. Not from Kloogh. From the news, in mid-2019, when the SFO involvement became public.

She went to the sideboard. She took out the folder. She looked at the most recent statement. The number was still there, the same number it had been when she filed it. The number had not changed. Only the world around the number had changed.

That part may be the saddest. The paper does not know it is lying. It sits in the drawer and continues to assert what it was printed to assert. The lie does not expire. It just stops being believed.

She is in her late seventies now. She still lives in Mosgiel. The folder is still in the sideboard, because she has not decided what to do with it. Throwing it out feels like admitting something. Keeping it feels like waiting for a different ending.

There is no different ending. The liquidator's letter will arrive eventually and put a final number on it. Two cents. Maybe less.

He said he was good with money management. He was. He managed it out of her drawer and into his own, one quarterly statement at a time, for twenty-six years.

The folder is still in the sideboard.

- Serious Fraud Office (New Zealand) | March 2020 | Charging documents and guilty plea announcement re Barry Edward Kloogh

- Serious Fraud Office (New Zealand) | 31 July 2020 | Sentencing announcement: 8 years 10 months, minimum non-parole 5 years 4 months

- Financial Markets Authority (New Zealand) | September 2019 | Cancellation of Kloogh's financial adviser authorisation

- Financial Markets Authority | October 2023 | "Lessons learned" report on the Kloogh case

- Official Assignee / Liquidator's report | 13 March 2026 | Recovery estimate revised to ~2 cents per dollar; $455,442 expected recovery from trust-linked property sales

- High Court of New Zealand | May 2023 | Judgment ordering $426,107 to official assignee, $40,823 to Svetlana Spectra

- Stuff (New Zealand) | 2026 | "Financial adviser convicted for 15m Ponzi scheme says he was 'good with money management'"

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.