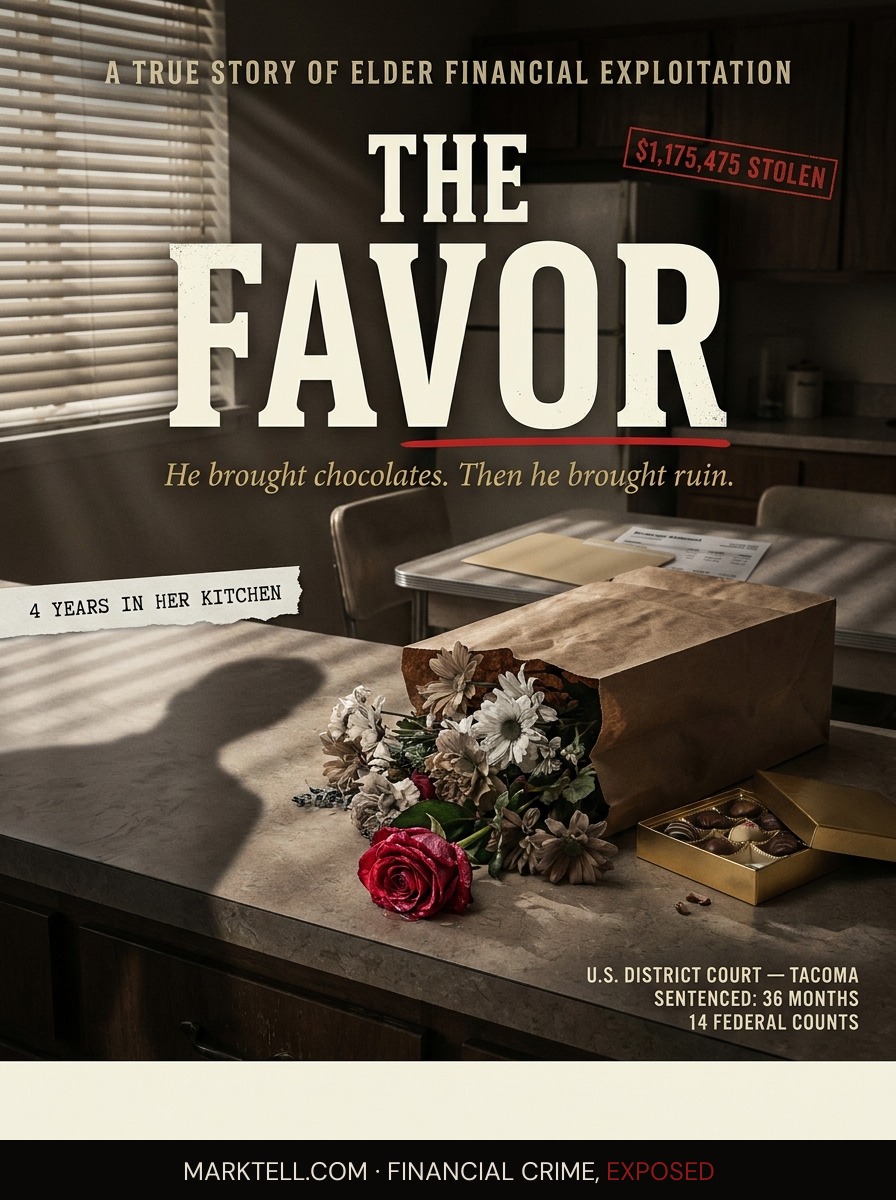

He bought her chocolates first. Then he bought an island home.

John S. Winslow spent four years moving a widow's life savings out of her brokerage accounts and into a hot tub, a new car, and an island home. The grocery runs were part of the structure.

Margaret was seventy-four and she lived alone.

Her husband had been dead nine years. The brokerage statements still came in his name and hers, and she kept them in a manila folder in the second drawer of the kitchen desk, the way he had taught her, in the order they arrived. She was not careless with money. She had been a careful woman her whole life. She just did not always remember, in the afternoon, what she had decided in the morning.

The man from the firm came by on a Tuesday with a grocery bag and a bouquet.

She had not asked him to. He said he was already at the store. He said the flowers were on sale. He set the bag on the counter and unpacked it himself, putting the milk in the door of the refrigerator and the bread on top of the bread box, the way somebody does who has been in your kitchen before.

This is how the four years started. Not with a pitch. With a grocery run.

His name was John S. Winslow. He was fifty-seven, licensed, employed by a national financial services firm, and her advisor of long standing. On May 13, 2026, in federal court in Tacoma, U.S. District Judge Tiffany M. Cartwright sentenced him to three years in prison and ordered him to pay $1,175,475 in restitution. The judge said the crime was personal. She meant that he had known the woman he was stealing from. He had been in her kitchen.

First Assistant U.S. Attorney Charles Neil Floyd put it in one line to the court.

"He meant to bleed her dry."

I.

The favor is the lock pick.

This is the part of elder fraud cases that does not show up cleanly on a wire transfer. The grocery bag. The chocolates. The ride to the doctor. The bouquet on the counter that nobody asked for. Each one of these things is a small kindness in isolation. Strung together over months, they become a credential. The advisor is no longer the advisor. He is the person who shows up. The person who shows up has access to the drawer where the manila folder lives.

According to the federal record, Winslow ingratiated himself with the widow by performing personal errands. Groceries. Flowers. Chocolate. Then, over roughly four years, he systematically moved funds out of her brokerage accounts at the firm and into outside bank accounts in her name. From there, the money went where he wanted it to go.

It went to an island home. It went to a hot tub. It went to a new car.

The victim, in the meantime, was living on a limited budget.

Read that again. The widow whose accounts he was draining was being kept on a fixed allowance, the way you keep a child on a fixed allowance, while the man with signature authority over her financial life was buying himself an island house.

II.

Here is how the path runs, in plain English.

A brokerage account is the account at a firm like Schwab or Fidelity or Morgan Stanley where stocks and bonds and mutual funds are held. It is regulated. It generates statements. Money does not leave it invisibly. To get money out of a brokerage account, somebody has to authorize a transfer, usually to a linked bank account.

Once the money lands in a regular bank account, it is easier to move. A bank account belongs to the named accountholder. If that accountholder is a seventy-something widow whose advisor has been doing her grocery shopping, and if that advisor is the one writing checks and initiating transfers because she has trouble remembering whether she paid the electric bill, the money does not need a second authorization to leave. It only needs a hand.

The federal indictment charged Winslow with four counts of wire fraud, two counts of mail fraud, four counts of money laundering, and four counts of making and subscribing a false tax return. Wire fraud is the use of electronic communications to carry out a scheme to defraud. Mail fraud is the same idea using the postal system. Money laundering is the act of moving the proceeds of a crime through accounts in a way designed to conceal where they came from. The false tax return counts are the part where he did not tell the IRS about the money he was stealing.

That is the machine. Brokerage to bank. Bank to lifestyle. Tax return left clean.

Four years.

III.

I want to stop here and say something about the firm.

The widow sued the national financial services firm that employed Winslow. The firm settled with her for $920,483. Under the sentencing order, that settlement amount is now what Winslow owes the firm in restitution, because the firm has already made her financially whole at that level. The firm fired him after the theft surfaced.

The firm has not been publicly named in the documents I have seen.

What a four-year drain on a single elderly client's brokerage account looks like inside a national firm is a question the public record does not fully answer. Brokerage firms have supervisory obligations. They have anti-money-laundering programs. They have systems that are supposed to flag unusual patterns of withdrawal from accounts owned by elderly clients. FINRA, the self-regulatory body for brokers, has spent years pushing rules specifically designed to catch elder financial exploitation. The whole architecture exists because this is the most common form of elder abuse: not a stranger on the phone, but a trusted person with access.

The settlement suggests the firm recognized some exposure. The amount of that exposure, and what their internal review found, is not on the public docket I can see.

That gap is where the question lives.

IV.

Picture Margaret in the kitchen.

The brokerage statements still arrive. They come in the same envelopes they have always come in. She opens them at the kitchen table because that is where her husband used to open them. The numbers on the statements have been going down for a while. She does not always remember what they used to say.

When she asks Winslow about it, he explains. He is patient. He uses words she understands. He has been her advisor for years. He brings chocolate.

This is the cruelty of cognitive decline as a fraud vector. The widow is not stupid. She has been careful her whole life. She is being targeted precisely because the mechanism the rest of us rely on to catch fraud, which is the ability to compare what we were told yesterday to what we are being told today, has become unreliable in her. Winslow knew that. The prosecution said so in court.

The IRS Criminal Investigation division worked the financial side. Special Agent in Charge Carrie Nordyke said the agency will keep pursuing people who do this. That is the public-facing line. The private fact is that for most of the four years Winslow was doing this, nobody outside that kitchen knew it was happening.

V.

The judge said the crime was personal. She was right about that, but it deserves a sharper word.

The crime was domestic. It used the architecture of care. The grocery bag was part of the structure. The bouquet was part of the structure. The chocolate was part of the structure. The hot tub on the island and the new car in the driveway were not the crime. They were the receipt.

The renaming matters here. We say "elder fraud" and the phrase sounds like a category. It sounds like the IRS phone scam and the gift-card grandparent scam and the Nigerian prince. Those are real, and they cost real money. But the form of elder financial exploitation that takes the most, and that the record keeps showing us, is not from a stranger. It is from somebody the victim knows by first name. A relative. A caregiver. An advisor. The person who shows up.

Federal estimates put elder financial exploitation losses in the billions every year. The single largest category, by repeated study, is theft by trusted persons.

Winslow got three years. He owes more than a million. The widow's accounts are restored, at least at the dollar figure she settled for. The hot tub will be sold or the home will be sold or some asset will be liquidated to satisfy restitution.

What does not get restored is the four years.

VI.

I keep thinking about the manila folder.

It is still in the drawer. The statements still come. Somebody else, a daughter or a niece or a court-appointed conservator, is opening them now. The numbers are going back up, slowly, because the settlement money has been wired in and is sitting in something safe.

Margaret is older than she was four years ago. She does not always remember the man who used to bring the chocolates. When she does remember him, she remembers him fondly, because the version of him she met first, the one with the grocery bag, was the one designed to be remembered fondly. That was the whole point.

He brought flowers because flowers are what you bring to somebody you are not stealing from.

The first thing he stole was the category.

- U.S. Attorney's Office, Western District of Washington | May 13, 2026 | DOJ press release on sentencing of John S. Winslow

- U.S. District Court, Western District of Washington (Tacoma) | May 13, 2026 | Sentencing hearing before Judge Tiffany M. Cartwright

- MyNorthwest.com | May 13-14, 2026 | "'He meant to bleed her dry': Fox Island financial advisor sentenced for $920K elder fraud"

- Federal indictment of John S. Winslow | approx. May 2025 | wire fraud, mail fraud, money laundering, false tax return counts

- FINRA | ongoing | rules and guidance on elder financial exploitation by registered representatives

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.