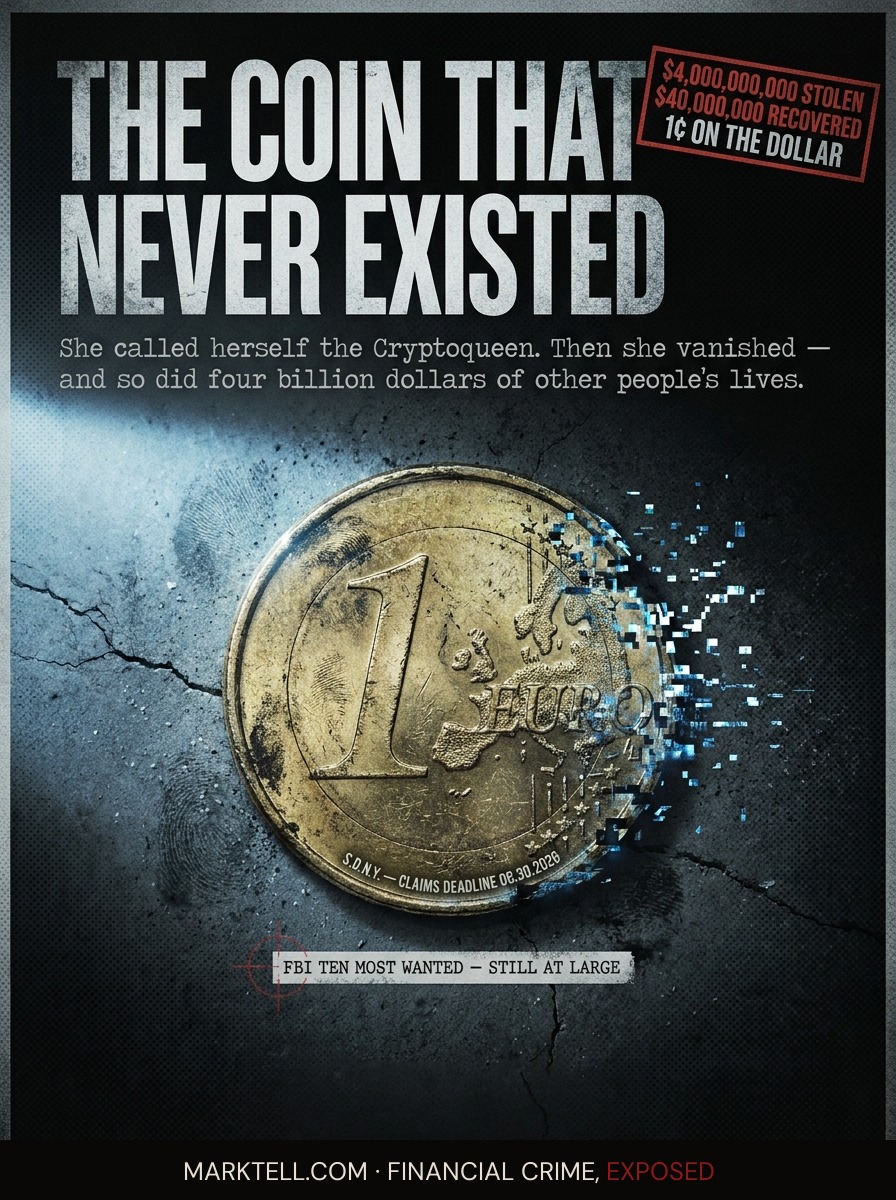

Four Billion Dollars Vanished. The Government Found Forty Million.

The Department of Justice just opened the compensation window for OneCoin victims, but the math is brutal before you even file a claim. Here is what actually happened to your money, where it went, and what forty million dollars means when four billion is already gone.

Picture the petition form.

It is two pages. Maybe three. It asks for your name, your country of residence, the amount you invested, the dates of your purchases. It asks for documentation. Bank transfers, receipts, account statements from a platform that no longer exists, from a company whose founders are either in prison or missing. The deadline is June 30, 2026. The website is www.onecoinremission.com. The administrator is a company called Kroll Settlement Administration LLC, a legitimate firm that processes exactly these kinds of claims, and the form is free to fill out, no lawyer required.

The form is real.

What it cannot do is fix the arithmetic.

Between 2014 and 2019, investors around the world put more than four billion dollars into OneCoin. Some estimates from researchers who tracked the global reach of the scheme put the figure closer to fifteen billion. The Department of Justice, in its prosecutions and forfeiture proceedings in the Southern District of New York, has confirmed the four billion figure. That is what the court record supports. Either number is large enough to restructure lives. Either number is large enough to empty retirement accounts, drain college funds, wipe out the savings that a family built over twenty years of night shifts and careful spending.

The compensation fund holds forty million dollars.

Do the math slowly. Not because it is complicated. Because the result takes a moment to land.

Forty million against four billion is one cent for every dollar lost. That is before Kroll processes the claims. Before the fund is divided among the estimated 3.5 million victims worldwide. Before the lawyers and administrators take their operational fees, which are standard and disclosed and still real. The FBI's own statement about this case used the word "monumental" to describe the losses. The gap between what was stolen and what is being returned is not a rounding error. It is the story.

And that story starts not in a courtroom in Manhattan, not in a DOJ press release, but in a language that most of the victims spoke before they ever heard the word OneCoin.

I.

Before anything else, you need to understand what OneCoin actually was. Not what it was sold as. What it was.

OneCoin was not a cryptocurrency. A cryptocurrency, in the functional sense, is a digital token that runs on a blockchain. A blockchain is a public ledger, a record of every transaction, maintained by thousands of computers simultaneously so that no single person or company can alter it. That distributed architecture, that inability to falsify the record, is the thing that gives legitimate digital currencies whatever value they have. The blockchain is the proof.

OneCoin had no blockchain. Not a flawed one. Not an experimental one. None.

The company maintained its own internal database, a private spreadsheet controlled entirely by the founders, where OneCoin balances were recorded. When you "bought" OneCoin, the number in that database went up. When the company decided the price had increased, the number next to your holdings went up too. The price was set manually, internally, by the same people who controlled the database. There was no market. There was no mining, the process by which legitimate cryptocurrencies use computing power to verify transactions and create new coins. There was no decentralization. There was a Bulgarian company in Sofia that decided how much your coins were worth each morning and typed that number into a spreadsheet.

This is not an allegation. This is what the court record describes. Multiple defendants have pleaded guilty to charges that include conspiracy to commit wire fraud and money laundering. Those guilty pleas contain factual statements, statements the defendants signed and agreed to as true, that describe exactly this architecture.

The blockchain was the credential that nobody checked.

Because the pitch did not require you to check. The pitch required you to believe.

And the pitch was very, very good.

II.

Amara was fifty-three when she first heard about OneCoin. She had spent most of her working life as a nurse, the kind of work that pays respectably but not generously, the kind of work where retirement requires planning that starts early and survives without interruption. By 2016 she had roughly sixty thousand dollars in savings. Not a fortune. Enough to matter.

She heard about OneCoin from a woman she trusted. That part is important. Not from an advertisement. Not from a cold call. From a woman she had known for years, a woman whose judgment she had reason to respect, who described an investment opportunity in cryptocurrency that was already making people serious money, that was growing faster than Bitcoin, that had a waiting list of buyers in certain markets because demand exceeded supply.

That last detail was fabricated. But fabrication and lie are not the same thing in a structure like this. The woman telling Amara about OneCoin was not lying. She believed it. She had bought in herself. She had watched her account balance climb inside the OneCoin platform. She had read the promotional materials. She had attended a presentation where men in expensive suits showed slides about blockchain technology and emerging markets and the democratization of finance. She had done her version of due diligence. She had satisfied herself that this was real.

The woman who convinced Amara was also a victim.

This is the architecture that makes a fraud like OneCoin different from a simple theft. Simple theft requires proximity. The thief needs to be near you. OneCoin built a multi-level marketing network, a structure where existing members earn commissions by recruiting new members, and the new members earn commissions by recruiting more members, layered downward until the base of the pyramid is wide enough to generate billions in inflows. In that structure, the recruiter is not a stranger. The recruiter is your nurse colleague, your church friend, your cousin who always seemed to find opportunities before everyone else.

The pitch came with warmth attached.

Amara was not stupid. She was not uninformed. She was operating in an environment designed specifically to defeat the defenses of a careful person. Every signal she had learned to trust, personal recommendation, visible success, professional-looking materials, enthusiastic community, pointed in the same direction.

She invested fourteen thousand dollars.

III.

Ruja Ignatova co-founded OneCoin in 2014. She had a doctorate in European private law from the University of Konstanz. She had worked for McKinsey. She wore tailored clothing and spoke six languages and stood on stages in front of thousands of people and described herself as building the cryptocurrency that would replace Bitcoin.

She called herself the Cryptoqueen. Her fans called her that too.

Karl Sebastian Greenwood, her co-founder, handled the network. The sales structure. The global MLM apparatus that moved money from Amara's bank account in one country through a recruiting chain that terminated somewhere near Sofia. Greenwood was arrested in 2018. In September 2023 he was sentenced to twenty years in federal prison. He was ordered to pay three hundred million dollars in forfeiture. The court record of his sentencing describes a man who understood exactly what OneCoin was and built the machine anyway.

Ignatova understood it too.

She disappeared in October 2017. She boarded a flight from Sofia to Athens. The trail goes cold there, though subsequent reporting and court filings suggest the sophistication of her exit, offshore accounts, false identities, jurisdictions selected for their opacity. The FBI placed her on its Ten Most Wanted Fugitives list. The U.S. State Department is currently offering up to five million dollars for information leading to her location and arrest. The FBI maintains a tip line. Eight years later, she has not been found.

Nobody outside the investigation knows exactly where she is. Not really. There are theories. There are reported sightings. There are filings in multiple jurisdictions describing assets that may be connected to her movement. But the woman who stood on stages telling investors she was building the future of money is somewhere in the world right now, and the people who gave her their savings do not know where.

Think about that for a moment. Not as an abstraction. As a fact that exists in the same week as the petition form.

IV.

Here is where the mechanics of a fraud like this stop being theoretical and start being physical. The money had to go somewhere. Four billion dollars does not evaporate. It moves. It gets layered, a term from money laundering that means the process of moving funds through multiple transactions and accounts to obscure where they came from, making it progressively harder for investigators to follow the chain.

Mark Scott was a partner at a major law firm. He was paid to build the infrastructure that moved more than four hundred million dollars out of OneCoin's network. He created investment funds, legal entities that appeared on paper to be legitimate private equity vehicles, funds that processed the OneCoin proceeds through banks in multiple countries. When investigators eventually unraveled those funds, the transactions had been structured specifically to avoid the reporting thresholds that would have triggered scrutiny. Scott was convicted in 2019. In January 2024, he was sentenced to ten years in federal prison.

Irina Dilkinska was OneCoin's Head of Legal and Compliance. She was extradited from Bulgaria and sentenced to four years in prison in April 2024. She was ordered to forfeit more than one hundred eleven million dollars.

Konstantin Ignatov, Ruja's brother, took over the operation after she disappeared. He was arrested at Los Angeles International Airport in March 2019. He pleaded guilty and cooperated with prosecutors. He was released in early 2024 after thirty-four months in custody.

Each of these people moved money. Each of these people touched the machine. The money they handled, the forfeiture judgments attached to their cases, contributed to the pool that became the forty million dollars now available for victims.

Forty million against four billion.

The math keeps returning to the same place.

V.

Amara filed her taxes the year after she invested. She listed the OneCoin purchase as an asset. By 2019, when the fraud became undeniable and the platform began restricting withdrawals in ways that should have been impossible if the coins had value, she understood that the asset was worth nothing. The tax situation became complicated. The documentation she had was incomplete. She had purchase confirmations sent to an email address she no longer controlled, on a platform she could no longer access.

This is not an edge case. It is the median experience.

A lawyer who has worked with OneCoin victims in the years since the fraud collapsed has noted publicly that the documentation requirement in the petition process creates an obstacle for victims who were operating in good faith but never anticipated needing to preserve a paper trail for a fraud claim. The June 30 deadline intensifies the pressure. Victims in countries where English is not the primary language face additional barriers. The burden of proof, under the petition rules, rests with the claimant.

The DOJ press release from April 13, 2026 states that victims are at the core of everything the department does. That is a statement of institutional mission, and it is sincerely meant by the people who made it. The FBI, the IRS Criminal Investigation division, the prosecutors in the Southern District of New York, the team that assembled the forty million dollar fund through years of forfeiture litigation in multiple jurisdictions, these are people who did serious work on behalf of the three and a half million individuals who were defrauded.

The forty million is real. The process is legitimate. The administrator is credible.

And one cent per dollar is still one cent per dollar.

Read that slowly.

Not because the government failed. Because the machine was built to survive the government finding it. By the time the law caught up with OneCoin, the money had been moving for five years through enough jurisdictions, enough fund structures, enough nominee accounts and correspondent banks and offshore entities, that most of it was functionally irretrievable. Greenwood's forfeiture order says three hundred million dollars. Scott's says the value of what he laundered. Dilkinska's says one hundred eleven million. The amounts ordered are not the amounts recovered. Forfeiture orders are not bank transfers. They are legal judgments that must then be enforced against assets that exist, in jurisdictions that cooperate, through processes that take years.

The difference between what the court ordered and what ended up in the compensation fund is not corruption. It is the structural reality of how money launderers operate. The gap is not accidental.

The gap is the product.

VI.

If you invested in OneCoin between 2014 and 2019 and you have not yet filed a petition, you have until June 30, 2026.

The website is www.onecoinremission.com. There is no fee to apply. You do not need a lawyer. The administrator, Kroll Settlement Administration LLC, can also be reached by phone at 1-833-421-9748. If documentation is a problem, file anyway. The instructions describe what is required and what alternatives may be accepted when records are incomplete.

Be careful about what comes next. Recovery scams, frauds that target people who have already lost money in a fraud by promising to recover those losses for an upfront fee, are common in the aftermath of large cases like OneCoin. The DOJ will never charge you a fee to access the remission process. Anyone who contacts you offering to navigate the petition process for a percentage of your recovery, or for any fee paid in advance, is running a secondary fraud against people who have already been through one.

The official contact is the website above and the toll-free number. That is the complete list.

If you are not sure whether what you have is legitimate, call the number before you pay anyone anything.

VII.

OneCoin was not the first cryptocurrency that was not a cryptocurrency. It was not the largest, by some estimates. It will not be the last.

The architecture of the fraud was not complicated. A database where you controlled the balances. An MLM network where recruiters were also victims. A charismatic founder who stood on stages and used the correct vocabulary in a moment when most investors did not yet know what the correct vocabulary even sounded like. A legal and compliance department that existed to legitimize rather than to govern.

These components are not specific to OneCoin. They are reproducible. They have been reproduced. Right now, somewhere, there is a platform with a convincing website and a whitepaper, which is a term for a document describing a cryptocurrency project's technical architecture and business model, that describes a revolutionary token with proprietary blockchain technology. The whitepaper will be long. The vocabulary will be precise. The community will be active and enthusiastic and full of people who believe they are building something real because they have watched their balance climb inside a platform they cannot withdraw from.

The tell is almost always the same.

Can you take the money out? Not in theory. Not according to the terms. Right now, today, if you tried to sell and move the proceeds to your bank account, what would happen? What does the process look like? Who controls it? What are the restrictions? What is the vesting period, the lock-up period, the withdrawal limit?

The question nobody wants to ask is the only question that matters.

Amara asked it in 2019. The answer was that withdrawals were currently limited due to regulatory compliance procedures being updated. The platform was working on it. Patience was requested. Community members were encouraged to stay the course.

She never recovered a dollar.

She is filing a petition before June 30.

One cent on the dollar is still something.

It is just not enough to be the end of the story. The machine that took her money is not in prison. Greenwood is. Scott is. Dilkinska is. The machine is a pattern, and patterns do not get sentenced. They get renamed. They find new vocabulary. They wait for the next moment when the technology is new enough that most investors have not yet learned to ask the ugly question.

Ruja Ignatova is somewhere in the world right now.

The coins she sold were never real.

The debt she left behind is.

- U.S. Department of Justice, Office of Public Affairs, "Justice Department Announces Compensation Process for OneCoin Fraud Victims With Funds Recovered Through Asset Forfeiture," April 13, 2026. https://www.justice.gov/opa/pr/justice-department-announces-compensation-process-onecoin-fraud-victims-funds-recovered

- U.S. Department of Justice, Southern District of New York, United States v. Karl Sebastian Greenwood, Sentencing, September 2023. Greenwood sentenced to 20 years, ordered to forfeit $300 million.

- U.S. Department of Justice, Southern District of New York, United States v. Mark Scott, Conviction 2019, Sentencing January 2024. Scott sentenced to 10 years for laundering over $400 million in OneCoin proceeds.

- U.S. Department of Justice, Southern District of New York, United States v. Irina Dilkinska, Sentencing April 2024. Dilkinska sentenced to 4 years, ordered to forfeit over $111 million.

- U.S. Department of Justice, Southern District of New York, United States v. Konstantin Ignatov, Guilty plea November 2019, cooperation agreement, released early 2024 after 34 months.

- FBI, Ten Most Wanted Fugitives List, Ruja Ignatova. Active listing. Reward: $250,000 via FBI. U.S. State Department reward: up to $5 million.

- Kroll Settlement Administration LLC, designated remission administrator for OneCoin victim compensation. www.onecoinremission.com.

- FBI Internet Crime Complaint Center (IC3), Internet Crime Report 2024, published April 2025. Investment fraud involving fictitious crypto platforms generated largest losses; Americans over 60 lost $1.83 billion from investment fraud, $2.84 billion total from digital asset scams.

- U.S. Department of Justice, Criminal Division announcement, April 2025: DOJ surpassed $12 billion in compensation to crime victims since 2000; over $735.3 million returned in fiscal year 2024 and early 2025.

- English High Court, claim filed January 2026 on behalf of 439 individual OneCoin victims; litigation funding agreement subsequently terminated.

- DOJ Asset Forfeiture Program, Criminal Division Money Laundering, Narcotics and Forfeiture Section (MNF), program history and mandate documentation.

Editorial Notice

MarkTell is a true crime publication about financial fraud. Some scenes, dialogue, and sequential details are reconstructed from court filings, enforcement actions, news reports, and public records. Where the public record does not provide exact details, editorial reconstruction is used to convey the documented pattern of events. Names of private individuals may be changed to protect identity. All factual claims are sourced to public documents cited in the Evidence Trail above. MarkTell does not provide investment, legal, or financial advice. Nothing published here constitutes a recommendation to buy, sell, or avoid any investment. Allegations described in active cases have not been adjudicated and defendants are presumed innocent until proven guilty. Readers should conduct their own due diligence before making financial decisions.